Federal Reserve increase rates; Mortgage Rates drop

Too often I see a headline like this one: “Mortgage Rates Continue to Slide Despite Fed Hike.” The 30-year Fixed Rate Mortgage (FRM) does NOT follow the Federal Reserve’s rate increases!

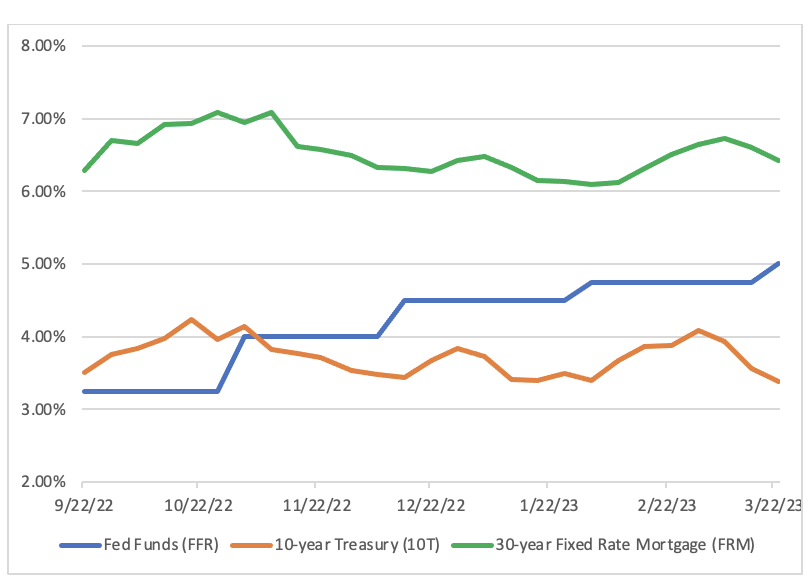

Look at this chart for the last few months:

Note the correlation between the 10T (red line) and FRM (green) – and the lack of correlation between FFR (blue) and FRM.

Let’s look at this another way, the spread (difference) between the FRM and 10T, and between FRM and FFR:

Over the last 6 months, the spread between FRM and 10T has been in a tight band between 2.69% and 3.04%, while that between FRM and FFR has dropped from 3.04% to 1.42%.

For a more detailed explanation of what drives mortgage rates – and why the FRM will fall at some point – read Why Mortgage Rates Will Fall

And these recent articles: (more…)

What drives Mortgage Rates in one chart

I can explain as often as I do that the 30-year Fixed rate Mortgage (FRM) is based upon the yield on the US 10-year Treasury (10T), not the Federal Reserve’s Fed Funds rate (FFR), but still I read regularly comments such as “mortgage rates will move up after the Fed increased its interest rate.”

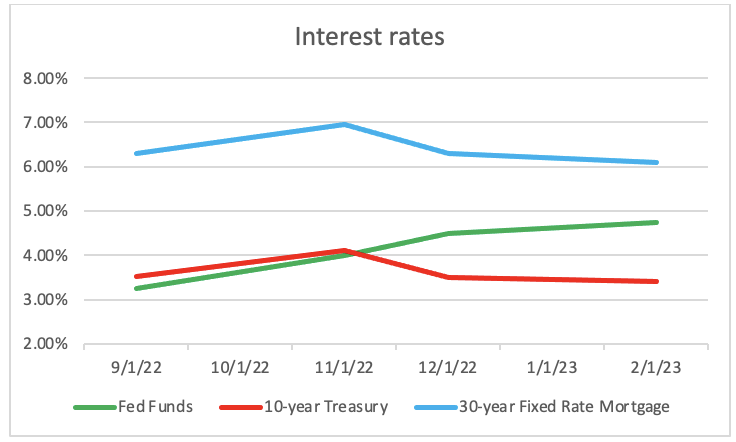

Look at this chart for the last few months, the dates being those when the Federal Reserve increased its interest rate:

Note the correlation between the 10T (red line) and FRM (blue) – and the lack of correlation between FFR and FRM.

Let’s look at this another way, the spread (difference) between the FRM and 10T and between FRM and FFR:

Over the last 5 months, the spread between FRM and 10T has been in a tight band between 2.69% and 2.85%, while that between FRM and FFR has dropped by a huge 1.7%.

For a more detailed explanation of what drives mortgage rates – and why the FRM will fall at some point – read Why Mortgage Rates Will Fall

And these recent articles: (more…)

Essex County 2022 Housing Market Review

Single Family Homes (SFH)

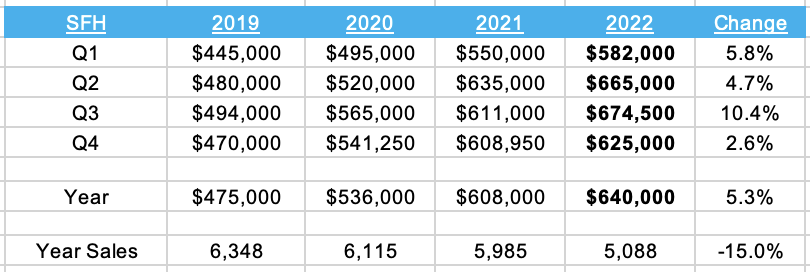

After sharp increases Year-over-Year (YOY) in Q2 and Q3, the median SFH price in Essex County showed a more modest increase (YOY) in Q4, and also showed the usual seasonal decline from Q3 into Q4. Overall, the median price increased 5% for the year to $640,000, taking the increase in the last 3 years to 35%. Reflecting the low levels of inventory recently, SFH sales declined 11% in H1 and 18% in H2.

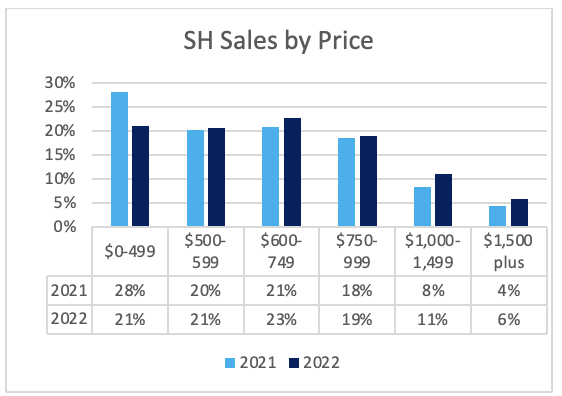

The share of sales over $600,000 increased from 52% in 2021 to 58% in 2022, driving the median price for the year well over $600,000.

Condos

The median condo sale price moved more steadily upwards in 2022, increasing by 11% in both H1 and H2, and by 34% since 2019. Sales fell 11% in H1 but by a startling 27% in H2. It seems likely that the increase in mortgage rates had a bigger impact on Condo sales – often bought as a first home with a significant mortgage – than on SFH sales, where mortgages – especially at the higher-end – tend to be less important with many buyers using cash or a large down-payment. (more…)

Why Mortgage Rates Will Fall

I have read and heard several comments suggesting that the increase in the 30-year Fixed Rate Mortgage (FRM) this year has been a direct result of the increase in the Federal Reserve’s Fed Funds rate (FF).

This is not correct.

As I will demonstrate, the FRM is determined by market forces, and in particular by the extra yield – the “spread” – which investors require when buying pools of mortgages (Mortgage Backed Securities or MBS), as compared with the risk-free yield available with the 10-year Treasury Note (10T) which has the nearest duration to the expected life of a pool of mortgages.

In contrast, the FF is the rate that banks use when setting their Prime Rates. When the FF increases, banks increase their Prime Rates and therefore the interest rate on those loans whose rates are based upon Prime Rates – e.g. credit cards and auto loans.

And we will see that the FRM increased this year long before the Fed started to increase the FF rate.

Mortgage-Backed Securities (MBS)

A conventional mortgage or conventional loan is any type of home buyer’s loan that is not offered or secured by a government entity. Instead, conventional mortgages are available through private lenders, such as banks, credit unions, and mortgage companies.

Most conventional mortgages are packaged into mortgage-backed securities and sold to investors. This allows the bank or originator to use its capital to finance more mortgages.

The relationship between 10T and FRM

This chart shows how the two have moved in lockstep over the last 30-plus years:

Source: National Association of Realtors

Mortgage Rates peaked? I spoke too soon

In June I published Have Mortgage Rates peaked? when the 30-year national average Fixed-Rate Mortgage (FRM) reached 5.81% and commented:”..a realistic expectation would be that the spread (the difference beyween the FRM and the yield on the 10-year Treasury) will drop from its current 2.5% to at least 1.8% at some point. If the yield on 10T stays in the low 3% range that would suggest that the FRM will drop below 5% again.”

Well it did…for a while, dropping to 4.99% on August 4th.

But then this happened:

Why have mortgage rates jumped again? (more…)

No, the Federal Reserve does not control mortgage rates

There is widespread misunderstanding about what drives mortgage rates. Indeed, I read an article recenlty on the National Association of Realtors website which stated that mortgage rates had risen sharply following the increase in the Federal Reserve’s interest rate.

Not so. (more…)

Have Mortgage Rates peaked?

With all the noise about the determination of the Federal Reserve (Fed) to continue to increase interest rates it might be tempting to asume that mortgage rates will continue to rise.

But I believe there are good reasons for thinking that mortgage rates may have peaked. Read on to find out why I think this.

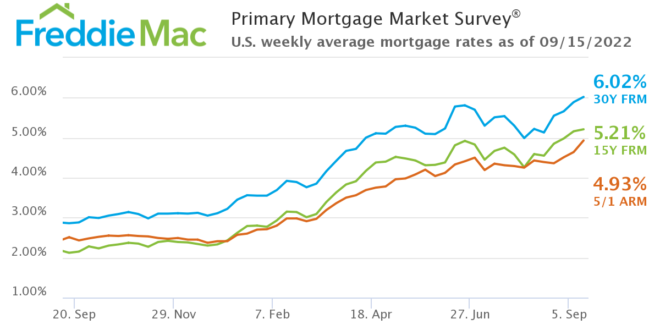

Current rates

The 30-year Fixed rate Mortgage (FRM) reached its highest level since 2008 this week: (more…)

What Higher Mortgage Rates Mean for the Housing Market

The recent uptick in mortgage interest rates is having a chilling effect on home buyers at the moment, but Wharton real estate professor Benjamin Keys doesn’t expect that to last.

Mortgage interest rates have increased across all categories in the last several weeks, following the Federal Reserve’s first rate hike since 2018 to fight inflation" haveeacroim2he moie lenu.st mmiibfec st es in fessmeek MorFdohro.slc