Twenty Questions with Marblehead’s Assessor

(Click here to download a pdf of this report.)

The FY2018 (July 1, 2017 – June 30,2018) tax rate has been set at $11.02, up a penny from $11.01 in FY2017. The median single family (SFH) assessment increased 4.3%, or $25,000, to $603,000, and the median single family tax bill increased 4.4%, or $281, to $6,645. The commercial rate has once again been set at the same level as the residential rate.

Note that the tax rate includes the cost of debt exclusions (mainly for school construction and the transfer station) voted by residents. These account for $1.12 of the 2018 tax rate, up from $1.07 in 2017. Excluding voter approved exclusions, the tax rate fell from $9.94 to $9.90.

Marblehead’s 2018 tax rate will be the second lowest of the 17 North Shore cities and towns and the fourth lowest of 34 Essex County communities. The highest rate in Essex County belongs to Amesbury at $18.99; the lowest Rockport at $10.11; and the median is $14.30. Swampscott’s residential rate for 2018 dropped from $17.45 to $16.00, while its commercial rate fell from $32.20 to $28.83.

Approximately 75% of Marblehead’s revenue comes from property taxes.

Real-estate assessments for Fiscal Year 2018 were mailed at the end of last year. Assessor Mike Tumulty answered questions about the process.

1. What is the time frame upon which assessments are based?

MT. For FY2018, assessments are based upon values as of January 2017, using sales data for calendar year 2016. Sales that took place in calendar year 2017, therefore, will be the basis for the assessment for FY 2019.

2. What percentage of properties sells each year?

MT. In 2016 there were 229 arms-length sales of SFHs, or 3.7% percent of the stock of 6,218, and 54 sales of condos, representing 5.5% percent of the stock of 984 units.

AO. While it is hard to get an accurate read on national statistics, it is certainly true that we stay in our houses longer than do people elsewhere. No surprise there: Marblehead is not only a great place to live, but it is also extremely well run, as demonstrated by our low tax rate.

3. Is there a minimum requirement for assessment purposes?

MT. The assessment process requirement is 2 % for each property class, or a minimum of 20 units. Where there are fewer than 20 sales, as in categories such as multi-families and commercial, data for 24 months is used. For FY 2018 that period is July 2015 to June 2017.

4. Can I appeal my assessment?

MT. Yes, provided the appeal is based upon data for the relevant year. More information and directions for filing an application are available at www.marblehead.org/assessors.

5. What is the process for appealing my assessment?

MT. An appeal for abatement can be made after receipt of the third quarter tax bill mailed in December and no later than Feb. 1. The appeal, which must be based upon valuation during the relevant period (i.e., 2016 calendar year sales for the current assessment), must specify the reason for the complaint. A current appraisal is not relevant. The assessor’s office will analyze the property and the information provided. If the data is incorrect or there is evidence provided that the valuation is wrong, the assessor’s office will change the valuation.

6. Does the assessment process include all transactions that occur?

MT. The process includes all arms-length transactions. Excluded are non-arms-length transactions, such as those involving foreclosure, bankruptcy, estate sales, divorce and the purchase and sale following remodeling.

7. What is the authority under which assessments are made?

MT. Chapter 59 of the Massachusetts General Laws. The process is overseen by the Department of Revenue.

8. How does Prop 2 1/2 affect assessments?

MT. The tax levy on all property in Marblehead in aggregate (not on individual properties) can be increased by no more than 2 1/2 percent per annum. To this total is added the tax on new growth (such as new construction, condo conversions, any improvements/parcels taxed for first time) and any overrides or debt exclusions, to calculate the new tax levy.

9. What are the measurements used in the assessment process?

MT. An assessment-sales ratio (ASR) is calculated for each property sold by dividing the current assessed valuation by the sales price. A property assessed at $100,000 that sold for $100,000 would have an ASR of 100 percent. If that property sold for $110,000, the ASR would be 91 percent ($100,000/110,000). If the property sold for $90,000, the ASR would be 111 percent ($110,000/100,000).

AO. Remember that the assessment is based upon data from earlier years, not the current year. A property that sold in January 2018, for example, would be assessed based upon data for the year 2016. If the market had risen in the last two years it would be reasonable to expect that the current market price would be higher than that on which the assessment was based. Thus in a rising market, the median ASR is likely to be less than 100 percent. Conversely, in a falling market, the median ASR is likely to be above 100 percent.

MT. A second factor is the “coefficient of dispersion,” which indicates how tightly the ratios are clustered around the median ratio. The lower the COD, the greater the uniformity in appraised values.

10. What are the state requirements for assessment values?

MT. The ASR for residential property must be in a range of 90-100 percent, and the COD must be no more than 10 percent. The ASR must be consistent throughout town for all types of property, both by classification – e.g. residential or commercial – and by price range. The purpose is to prevent one class of property subsidizing others.

11. What are Marblehead’s goals?

MT. An ASR of 95 percent. With a COD of 10 percent, that means that the range of ASRs should be 90-100 percent. Bear in mind that these are the values at the time the assessments are made. The actual ASRs at the time of sale will vary depending upon market conditions.

12. How did Marblehead do last year?

MT. For both Single Family Homes (SFH) and Condos the ASR was 98% and COD less than 4.5%.

AO. These numbers apply to the entire stock of housing and are medians, but the results speak to the overall accuracy of assessments.

13. How big is Marblehead?

MT. 4.2 square miles with 14 miles of coastline and 30 residential neighborhoods.

14. What happens when property changes hands — what does the assessor’s office do?

MT. The assessor’s office receives data on all sales and sends out a questionnaire (which is completed by 80 percent of buyers) to the new owner. This data provides background information and is taken into account for subsequent assessments.

15. What happens when improvements are made?

MT. The assessor’s office receives copies of all building permits and visits every site for which a permit is pulled. The assessor’s office determines the progress of work as of July 1, regardless of the status at the building department.

16. Which improvements have the greatest/least impact on assessed values?

MT. The greatest: new construction, additions, bathroom and kitchens. The least: those that minimize deferred maintenance: siding/roofing/windows — items that are expected and integral to functionality and habitation

17. How does Marblehead tax commercial property?

MT. Each year, the assessor’s office presents to the Board of Selectmen a schedule showing the impact of implementing a commercial rate that is allowed, by law, to be higher than the residential rate. In Marblehead, 95 percent of property is residential, so the imposition of a separate, higher commercial rate would have a disproportionate impact on commercial taxes. Indeed, if the share of the tax bill paid by commercial owners were increased by the maximum 50 percent, the reduction in the tax paid by the median homeowner would be just $187 per annum, while the increase on a similarly assessed commercial property would be $3,323.

18. Are there exemptions available?

MT. Statutory exemptions, for which the town is reimbursed by the state, are available for eligible taxpayers and include exemptions for the elderly, veterans, the blind and widows. More information on exemptions is available from the assessor’s office, 781-631-0236, or e-mail, assessors@marblehead.org. Please take advantage of those for which you are eligible.

19. How does the senior work-off program work?

MT. Opportunities for duties such as filing, phone coverage and light clerical work are available for senior citizens through the Senior Work-off Program. Seniors over 60 who meet certain income guidelines can earn a rebate on their taxes of up to $750. Applications for this program go through the Council on Aging office on Humphrey Street, 781-631-6737.

20. What is the outlook for 2019 assessments and tax rates?

AO. The FY 2019 assessments will be based upon sales in 2017, when the median price of sales reported in MLS increased 7% to $665,000.

It is likely, therefore that assessed values will be going up in FY2019, a year in which debt service costs may fall, a combination that should lead to the tax rate dropping below $11 in FY2019.

Why have mortgage rates spiked?

(Click here to download a pdf of this report.)

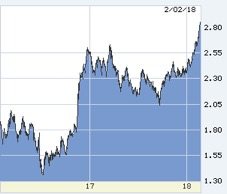

While the Freddie Mac weekly survey for the 30 year Fixed Rate Mortgage (FRM) this week showed an increase of just 0.07% to 4.22%, that survey was based upon rates in the early part of a week which saw a major upward move in the yield on the US 10 year Treasury (10T). As regular readers of this blog know, the rate of the FRM is closely tied to the yield on 10T. Here is a recent chart of the 10T.

The yield on 10T started 2017 at 2.45% and ended it at 2.40%, but in 2018 it has jumped, in just five weeks, to 2.84%.

It is likely that the coming week will see Freddie Mac’s survey number come in close to 4.5%, after spending most of 2017 under 4%.

Why has the yield on 10T – and hence the rate of the FRM – suddenly spiked?

I’ll answer that with bullet points:

1. 10T reflects economic activity and expectations and the economy has been growing quite rapidly and now is being boosted by significant tax cuts.

2. Those tax cuts will add $1.5 trillion to the budget deficit, a sum that will need to be financed largely by selling Treasuries.

3. Historically low unemployment levels have not translated into higher wages – until now, with the annual increase reaching 3%.

4. The seeming lack of wage pressure led many to believe that inflation had been contained, and that the old economic belief that easy money would lead to higher inflation no longer held true. That complacency has been rudely shaken in the last few weeks.

5. After many years when the Federal Reserve was a major buyer of Treasuries, it is now a seller and increased its pace of sales in January.

6. In 2018 the Treasury will be increasing the amount it will be raising at a time when one of the major buyers – the Federal Reserve – has reversed direction.

7. For the first time in a long while, Europe is showing economic growth at the same time as the US, and the European Central Bank has also started to reduce its buying of Government Securities.

8. The dollar has been very weak in recent months, something which does not encourage foreign buying of US Treasuries.

The Federal Reserve has the twin mandates of maximizing employment and stabilizing prices, although recently the Fed has said it wants to see inflation of 2%. The Fed has already increased short-term rates 5 times and has forecast 3 more rate increases for 2018.

All in all, there is quite suddenly a lot of uncertainty and concern creeping into markets, as we saw with the sharp sell off in the stock market on Friday. In today’s world events can move very quickly, as we have seen with interest rates in 2018. Barring an unforeseen event which causes an economic slow down, it does seem that the era of easy and cheap money has ended.

For more detail about the impact of interest rates on mortgage rates read Why mortgage rates may be headed upwards – finally which I published last October.

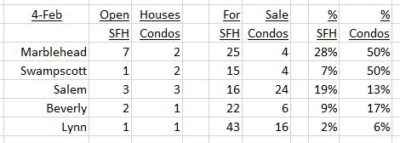

Super Bowl Sunday Open Houses

Let’s hope the Patriots score more points tonight than the total of Open Houses in Marblehead, Swampscott, Salem, Beverly and Lynn:

Harborside Sotheby’s International Realty

Marblehead Open Houses

Swampscott Open Houses

Salem Open Houses

Beverly Open Houses

Lynn Open Houses

GO PATS!

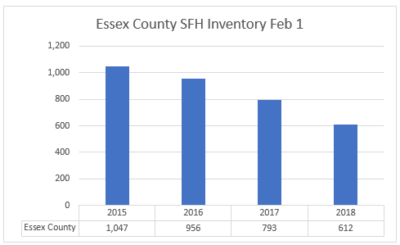

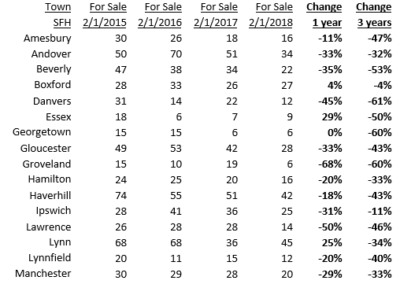

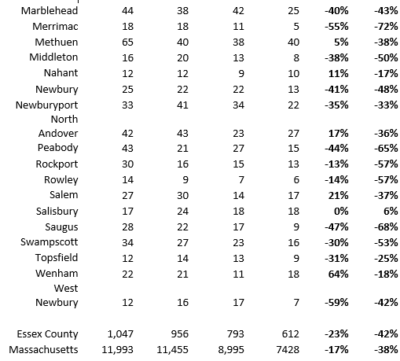

Housing Inventory continues to shrink

The number of Single Family Homes (SFH) for sale in Essex County as of February 1 is down 23% from a year ago and down 42% compared with 2015.

The chart below shows the overall numbers for Essex County and Massachusetts, followed by tables for each city and town.

OliverReports.com

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact Andrew Oliver on 617.834.8205 or Kathleen Murphy on 603.498.6817.

If you are looking to buy, we will contact you immediately when a house that meets your needs is available. In this market you need to have somebody looking after your interests.

Are you thinking about selling? Read Which broker should I choose to sell my house?

Andrew Oliver and Kathleen Murphy are Realtors with Harborside Sotheby’s International Realty. Each Office Is Independently Owned and Operated

@OliverReports

Lynn 2017 Housing Market Review

(Click here to download a pdf of this report.)

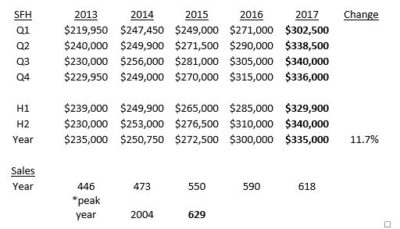

The median price of the SFHs sold in Lynn in 2017, after reaching $300,000 for the first time in 2016, increased by 11.7% to $335,000. This took the gain to over 40% since 2013. Sales continued their recent climb and were within a whisker of the record set in 2004.

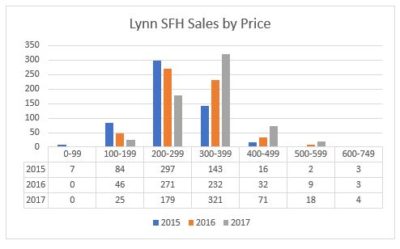

There has been a dramatic change in the number of houses sold at lower prices, with the number under $200,000 dropping from 91 in 2015 to just 25 last year. There was also a big drop last year in sales under $300,000 and a jump in sales above that figure, all evidence of quite rapidly rising prices.

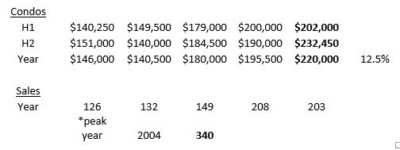

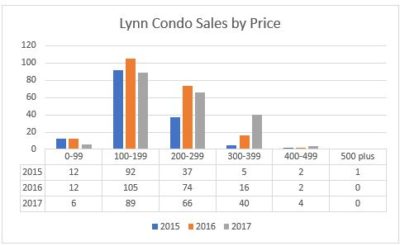

Condos

A 12.5% increase in the median price saw it break through $200,000 for the first time, finally eclipsing the 2006 peak. The gain occurred in the second half of the year. Sales maintained the 2016 pace but remain well below the 2004 level.

Sales under $200,000 have declined while there has been a sharp increase in sales over $400,000.

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact Andrew Oliver on 617.834.8205 or Kathleen Murphy on 603.498.6817.

If you are looking to buy, we will contact you immediately when a house that meets your needs is available. In this market you need to have somebody looking after your interests.

Are you thinking about selling? Read Which broker should I choose to sell my house?

Andrew Oliver and Kathleen Murphy are Realtors with Harborside Sotheby’s International Realty. Each Office Is Independently Owned and Operated

@OliverReports

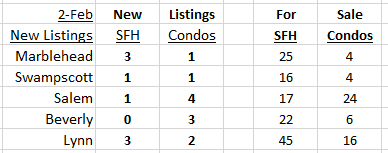

New Listings week ending February 2

Searching for a synonym for trickle I came up with dribble or drop. So this is the week’s dribble of new listings:

Harborside Sotheby’s International Realty

Marblehead new listings

Swampscott new listings

Salem new listings

Beverly new listings

Lynn new listings

Recent Comments