What drives Mortgage Rates – and no it’s not the Federal Reserve

I am always astonished by the number of reports I read, before and after the Federal Reserve (Fed) makes a change in its interest rate, about the effect such a change will have on mortgage rates.

No doubt it came as a surprise to those writers when there was virtually no change in the Freddie Mac weekly survey of mortgage rates this week.

Myth

“Mortgage rates react to the Fed.”

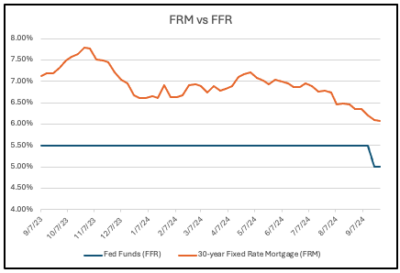

Look at this chart for the last year:

The FFR rate was unchanged at 5.5% for over a year until last week, but during that time frame the FRM varied between a high of almost 7.8% last October and a low of just over 6% last week before the Fed cut its inetrest rate by 0.5%.(The Freddie Mac survey takes place from Monday-Wednesday each week, so the 6.09% reported on September 19 reflected rates before the Fed cut its interest rate).

What happened after the Fed cut rates?

Precious little. The rate before the Fed cut rates was 6.09% and afterwards…. 6.08%.

In simple terms, there is no correlation or link between the Fed’s interest rates and the rate on 30-year Fixed Rate Mortgages.

What does determine Mortgage Rates? (more…)

The Federal Reserve’s new buzzword: Recalibrate

At Wednesday’s press conference after the Fed – finally – cut rates by 50 basis points (bp)(0.5%) – Fed Chair Powell introduced a new phrase to explain their action: “recalibrate.”

We have been through “transient inflation”; “data dependent”; “higher for longer”; and “data-dependent, not data point dependent” and have reached “recalibrate”.

Chair Powell denied that they were playing catch up because they waited too long to start cutting rates (they are, and they did).

Frankly, after their slow and deliberate approach this year, I expected only 25 bp. BUT…the next meeting is not until November 6, the day after the Election. And who knows what the environment will be on that date? It is certainly not out of the question that there will be a lack of clarity about the outcome. And while the Fed states that it not influenced by political considerations, they will naturally be aware of an environment which may well make it difficult for them to make an accurate forecast of the future.

So 50 bp now is “not a catch up” – but it would have been more consistent – and raised fewer questions – if they had cut 25 bp in July and a further 25 bp now.

Mortgage rates

I will update my 2023 article Why Mortgage Rates will fall in 2024 in the next few days. In that article I predicted that the 30-year Fixed Rate Mortgage (FRM) would drop below 6% by the end of 2024. I also explained why mortgage rates do not follow the Federal Reserve’s interest rate decisions, but are market driven based on the yield of the 10-year Treasury.

And to make to make that point more clearly: in both Massachusetts and Florida it is already possible to get FRMs for 5.5%, a sharp drop from from earlier in the year.

Also read:

The Federal Reserve’s Analysis Paralysis

Federal Reserve Chair Powell:”The Time has Come”

Federal Reserve Chair Powell:”The Time has Come”

“The time has come,” the Chair announced,

“For easing to begin—

From tightening strings, and cautious holds—

And dovish, hawkish spin

And then the market breathed a sigh—

When at last the Fed gave in.”

Read:

Earth to Federal Reserve: What are you waiting for?

The Federal Reserve’s Analysis Paralysis

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact me on 617.834.8205 or [email protected].

Andrew Oliver, M.B.E.,M.B.A.

REALTOR®

m 617.834.8205

www.OliverReportsMA.com

““If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReportsMA.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

“Thank you for the wonderful, wonderful job you do for the community (explanation of property tax process and calculation) – it is so helpful and so clearly explained.”

Licensed in Massachusetts with Stuart St.James

Licensed in Florida with Compass

www.OliverReportsFL.com

Earth to Federal Reserve: What are you waiting for?

This is the same headline I used in February 2022 in this article, when the Federal Reserve (Fed) was dithering about raising rates. It is just as applicable today as they dither about cutting rates.

Indeed, sometimes I wonder if the Fed is more concerned about coming up with catchy phrases: “transient inflation; “data dependent”; “higher for longer”; and now “data-dependent, not data point dependent” – than actually taking decisions.

“Date-dependent mean the Fed doesn’t have a clue”

This was a heading in an earlier Bloomberg article, which continued: But perhaps the bigger takeaway is that Chair Jerome Powell and his fellow policymakers really don’t have a clue what’s going to happen in the economy. They’re shooting in the dark. “They’re making it up as they go along.”

These comments may seem harsh but it expresses the frustration many feel about what I described in this recent article: The Federal Reserve’s Analysis Paralysis

The data is unreliable and subject to change

Mohamed El-Erian, whom I often quote, captured the current state of affairs when he observed: “I think the major issue is that the market has become overly data-dependent, just like our central banks have become overly data-dependent. So, we’re not looking beyond the next data release because we’re worried about what will the Fed do in September, what will the ECB (European) Central) Bank) do in September.”

Central bankers and markets should be aware of the risks associated with an overly data-dependent approach to monetary policymaking. In 2019, Powell himself highlighted the basic challenge: “We must sort out in real time, as best we can, what the profound changes underway in the economy mean for issues such as the functioning of labor markets, the pace of productivity growth, and the forces driving inflation.”

Yet economic data are often unreliable. Official statistics undergo multiple and often substantial revisions. For instance, the payroll numbers undergo subsequent revisions —sometimes large ones that give the lie to the initial perceptions.

Richard Fisher, a former Dallas Fed president, once offered an example of the dangers involved. Data pointing to excessively low levels of inflation had prompted the Fed to keep rates low in 2002 and 2003. Subsequent revisions, he acknowledged, showed that “inflation had actually been a half point higher than first thought. In retrospect, the real fed funds rate turned out to be lower than what was deemed appropriate at the time and was held lower longer that it should have been.”

In a recent Financial Times article, Mohammed-El Erian asked a number of questions, amongst them:

Why did Fed forecasts get it so wrong, be it on inflation or unemployment — the so-called dual mandate — in recent years? And to what extent has this resulted in a longer-term shift to excessive data dependency in the formulation of the central bank’s policy?

Ongoing structural and secular changes in how the US and global economies function are more consequential for policy design than “noisy” short-term data. So, is it not now time to combine data dependency with a much greater injection of forward-looking strategic thinking? (more…)

The Federal Reserve’s Analysis Paralysis

In November 2023, I wrote: “The question now is whether the Federal Reserve, having been extremely slow to start raising rates and reversing Quantitative Easing, will be similarly late in easing (rates). The Fed claims to be data dependent, but data tells us what happened in the past – and the Fed’s actions impact the future.”

The answer to that question is “yes” – and here we are, 8 months later, and the Fed is still “data dependent”, although this year’s mantra has become “higher for longer.”

2022

While nearly everybody outside the Fed now accepts that it kept interest rates “too low for too long”, I published the following articles: (more…)

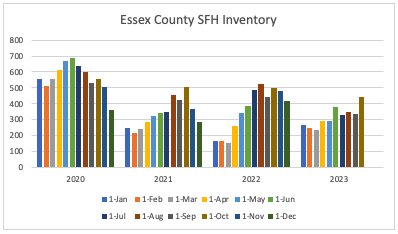

March Inventory shows no Improvement

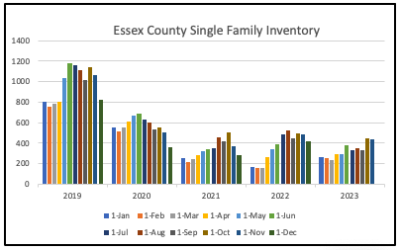

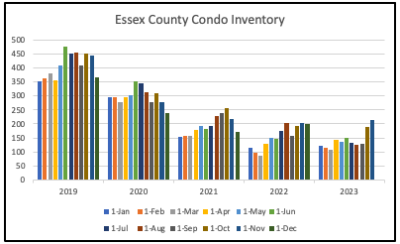

Overall in Essex County, while Inventory has been reasonably consistent in the last 3 years, it is running at less than half the 2020 levels for both Single Family Homes and Condos.

Single Family Homes (SFH)

Condos

Mortgage rates (more…)

December Inventory shows little change, while mortgage rates fall

Overall in Essex County, while Inventory has been reasonably consistent in the last 3 years, it is running at around half 2019 levels for both Single Family Homes and Condos.

Single Family Homes (SFH)

In the early months of 2023 SFH was up 50% or more from the extremely low levels in 2022. By the summer, YOY inventory was down by around 1/3. October showed an increase of 1/3 from September 1. In December inventory was above 2021 levels- but that was in the early staages of the COVID-buying surge.

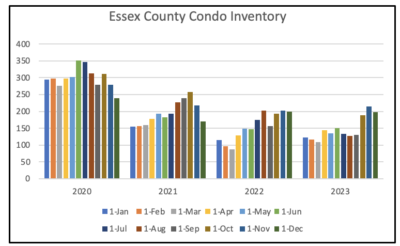

Condos

Condo inventory has increased sharply since the estremely low levels of August.

Mortgage rates

As inflation has slowed significantly this year (read Core Inflation Prices Barely Budged in August), the Federal Reserve finally stopped hiking rates. Meanwhile, the yield on the 10-year Treasury (10T) – which influences mortgage rates – soared in recent months, in part as the market has realised that there will be record sales of Treasuries at a time when the Federal Reserve has tuned seller, and foreign countries are not increasing their holdings and purchases of Treasuries. (more…)

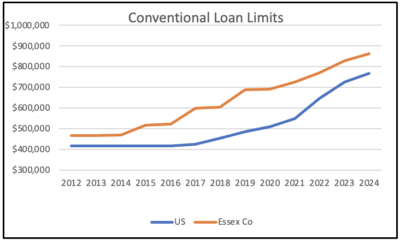

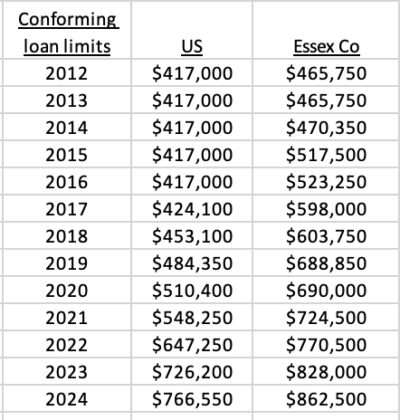

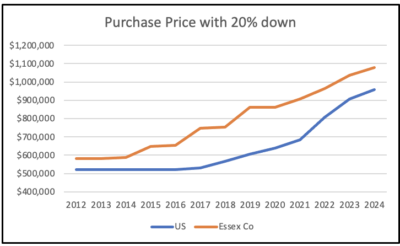

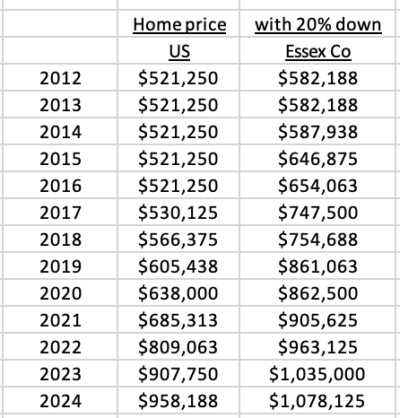

Conventional Mortgage Loan Limits increased for 2024

Fannie Mae and Freddie Mac are restricted by law to purchasing single-family mortgages with origination balances below a specific amount, known as the “conforming loan limit” (CLL) value. Loans above this amount are known as jumbo loans.

Essex County is considered a high-cost area, and limits are higher than the base level set by the FHFA. For 2024, the CLL is $766,550 and for Essex County the limit is $862,500,

Which means that, with a 20% down payment, a property in a standard area costing just over $950,000 can be purchased with a conventional mortgage, and in Essex County that rises to well over $1 million.

And these recent articles:

Why Mortgage Rates will fall in 2024

Conventional Mortgage Loan Limits increased for 2024

INFLATION and RECESSION UPDATE

Most Sales Still Over List Price

Core Inflation Prices Barely Budged in August

MARBLEHEAD Q3 MARKET REPORT 2019-2023

SWAMPSCOTT Q3 MARKET REPORT 2019-2023 SALEM Q3 MARKET REPORT 2019-2023

ESSEX COUNTY Q3 2023 MARKET REPORT

(more…)

INFLATION and RECESSION UPDATE

This time last year, stocks were still in the gutter, inflation was in the stratosphere and Fed interest rates were going up, up, up. Today the S&P 500 has risen 17% since Jan. 1, the much-anticipated recession has yet to arrive, unemployment remains below 4% and consumers are still spending–Walmart, Target, and Gap all beat expectations this week.

Inflation has dropped to around 3%, not too far off the Fed’s 2% target. Walmart CEO Doug McMillon was talking about deflation in the coming months. Oil prices are below $75 a barrel, Airfares are significantly cheaper this year than they were for the holidays last year. Bond yields are dropping, too, as traders start to price in Fed rate cuts next year. The 10-year yield has dropped back to around 4.4% from as high as 5% in October. (Barrons)

On Thursday, Walmart CEO Doug McMillon said deflation could be coming as general merchandise and key grocery items, such as eggs, chicken and seafood get cheaper.

He said the retailer expects some of the stickier higher prices, such as the ones for pantry staples, to “start to deflate in the coming weeks and months,” too.

“In the U.S., we may be managing through a period of deflation in the months to come,” he said on the company’s Thursday earnings call. “And while that would put more unit pressure on us, we welcome it, because it’s better for our customers.”

“I think the most important observation we’ve made is that the worst of the inflationary environment is behind us,” Hone Depot, Chief Financial Officer Richard McPhail

The question now is whether the Federal Reserve, having been extremely slow to start raising rates and reversing Quantative Easing, will be similarly late in easing. The Fed claims to be data dependent, but data tells us what happened in the past – and the Fed’s actions impact the future.

“The Fed must lower rates to cause money suply to grow by 5% per year, consistent with the 2% inflation target.If the Fed waits until core inflation is 2% we could have a recession.”(Jeremy Siegel, Wharton) (more…)

Why Mortgage Rates will fall in 2024

This article addresses two things: what drives mortgage rates, and why they will fall in 2024.

What drives mortgage rates?

The Federal Reserve (Fed) meets regularly and announces, with great fanfare, its “Federal Funds Rate(FFR).” But what is this interest rate and what does it influence?

The FFR is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. It is this rate which impacts the interest rate on many consumer loans, such as credit cards and automobile loans, but NOT 30-year Fixed-Rate Mortgages (FRM).

In general, FRM are sold to Fannie Mae and Freddie Mac and are bundled into portfolios which are sold to investors as Mortgage-Backed Securities (MBS). The yield investors demand for MBS is based upon the yield on the US Treasury 10-year (10T) yield, and the extra yield investors want to buy MBS rather than just risk-free Treasuries.

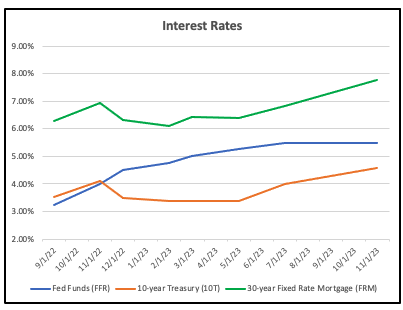

Look at this chart showing the three rates (FRM, FFR and 10T) over the last year. Note that the Green (FRM) and Red (10T) lines move in tandem, while the blue line (FFR) does not move with either of the other two. Thus, the FRM is determined by the yield on 10T, which is set by the market, and not by the Federal Reserve.

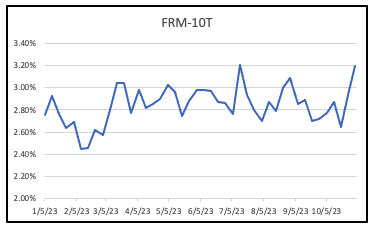

The Spread

The spread – reflecting the extra yield investors want to buy MBS – between FRM and 10T this year has between 2.5% and 3.2%. That is unusually high, as we shall see.

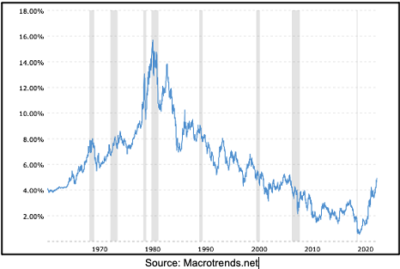

Why Mortgage rates will Fall

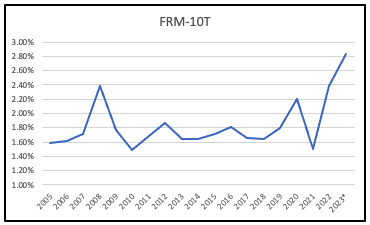

And now to the forecast. The spread between FRM and 10T is much higher than it is in “normal” times. Look at this chart going back to 2005:

For most of the last 18 years the spread has been in the 1.6 – 1.8% range and has averaged around 1.75%. The exceptions have been:

2008 – the Great Recession and the height of the foreclosure crisis making mortgages unattractive to investors, who demanded higher yields

2020 – at the outset of the pandemic, amidst widespread uncertainty, spreads widened before the Fed started its huge program of pouring money into the economy, buying both Treasuries and MBS and igniting an asset boom

2022-23 – when the Fed finally, belatedly, stopped injecting liquidity into the system, the market reacted to two main factors: the Treasury would need to sell a lot more Securities to fund the spending, and the growing Budget deficit; and the fact that the biggest buyer of Treasuries – the Fed itself – was switching from being a buyer to a seller.

This resulted in the most basic economic equation – more sellers than buyers, so the price of Treasuries went down and the yield (which moves inversely to the price) went up.

How far will mortgage rates fall?

Few if any forecasts have been accurate over the last few years, so it would be foolish for me to suggest a timeframe.

What is less foolish is to suggest that the era of cheap money over the last 15 years has ended. It is only in that period that the yield on 10T has been below 4%, and a sustained return to a 4% yield on 10T is likely.

That in turn would suggest a sub 6% FRM.

Not 3%, but better than 7.7%.

And these recent articles:

Most Sales Still Over List Price

Core Inflation Prices Barely Budged in August

MARBLEHEAD Q3 MARKET REPORT 2019-2023

SWAMPSCOTT Q3 MARKET REPORT 2019-2023

SALEM Q3 MARKET REPORT 2019-2023 (more…)

November Inventory down 60% from 2019

Overall in Essex County, while Inventory has been reasonably consistent in the last 3 years, it is running 60% below 2019 levels for Single Family Homes and 50% below for Condos.

Single Family Homes (SFH)

In the early months of 2023 SFH was up 50% or more from the extremely low levels in 2022. By the summer, YOY inventory was down by around 1/3. October showed an increase of 1/3 from September 1. By November inventory was above 2021 levels- but that was in the early staages of the COVID-buying surge.

Condos

Condo inventory has increased 70% since August,taking it back to 2021 levels.|

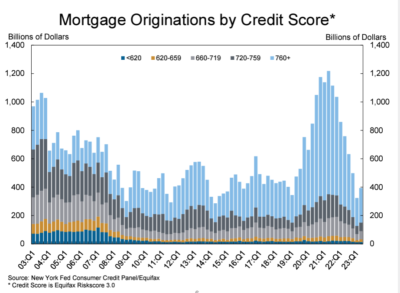

Two More Ways the Mortgage Market differs from 2007/2008

The chart below shows how loans with a credit score under 660 – the bottom colours of yellow and dark blue – which were about 20% of the total in the 2004-2007 period, have virtually ceased, with loans over 720 now making up the vast majority of new mortgages.

Two other changes:

Adjustable-rate mortgages can lead to higher default rates when interest rates rise, but they now represent less than 5% of total purchase and refinance loans, compared with over 35% at the peak of the pre-GFC (Global Financial Crisis) housing cycle. (FORTUNE)

The ratio of Americans’ mortgage debt to their real estate assets—also called loan-to-value—was just 27% in the second quarter, compared to over 40% in 2008 and roughly 50% in 2010. (Bank of America)

And these recent articles:

Core Inflation Prices Barely Budged in August

Two More Ways the Mortgage Market differs from 2007/2008

October Inventory shows Sharp Jump from September

Credit Score Change Could Help Millions of Buyers (more…)

October Inventory shows Sharp Jump from September

Overall Inventory in Essex County has been on a roller-coaster this year in terms of comparison with a year ago.

Single Family Homes (SFH)

In the early months SFH was up 50% or more from the extremely low levels in 2022. By the summer, YOY inventory was down by around 1/3. October showed an increase of 1/3 from September 1, bringing the YOY deficit to just 11%.

Condos

Condo inventory showed a similar, if less exaggerated, pattern. The 45% increase from September to October brought inventory levels in line with 2022’s, but still well below those in 2020 and 2021.

(more…)

Core Inflation Prices Barely Budged in August

While inflation rose 3.5% year-to-year in Aug. – still above the Fed’s 2% goal – it was only up 0.1% month-to-month after backing out higher gas prices.

Core inflation slows

But excluding the volatile food and gas categories, “core” inflation rose by the smallest amount in almost two years in August, evidence that it’s continuing to cool. Fed officials pay particular attention to core prices, which are considered a better gauge of where inflation might be headed.

Core prices rose just 0.1% from July to August, down from July’s 0.2%. It was the smallest monthly increase since November 2021.

Compared with a year ago, core prices were up 3.9%, below July’s reading of 4.2%. That, too, was the slowest such increase in two years. (more…)

Credit Score Change Could Help Millions of Buyers

The nation’s consumer bureau took a first step to erase medical debt from credit reports and lending decisions because that type of debt “has little predictive value.”

The Consumer Financial Protection Bureau (CFPB) outlined proposals under consideration – moves that it says would help families recover from medical crises, stop debt collectors from coercing people into paying bills they may not owe, and ensure that creditors don’t rely on data that is often plagued with inaccuracies and mistakes.

“Research shows that medical bills have little predictive value in credit decisions, yet tens of millions of American households are dealing with medical debt on their credit reports,” says CFPB Director Rohit Chopra. “When someone gets sick, they should be able to focus on getting better rather than fighting debt collectors trying to extort them into paying bills they may not even owe.”

“Access to health care should be a right and not a privilege,” Vice President Kamala Harris told reporters as she helped CFPB make the announcement. “These measures will improve the credit scores of millions of Americans so that they will better be able to invest in their future.” (more…)

Recent Comments