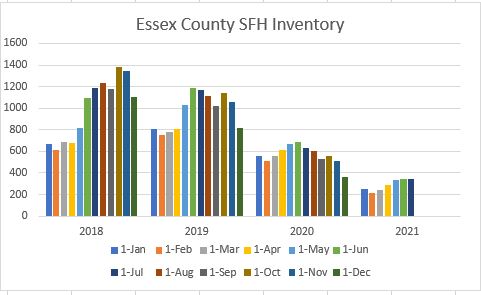

Housing Inventory little changed in July

Housing inventory for the 34 cities and towns of Essex County in pictures. Note that not only are numbers low but that there was no pick-up in the spring/summer market:

Single Family Homes

Condos (more…)

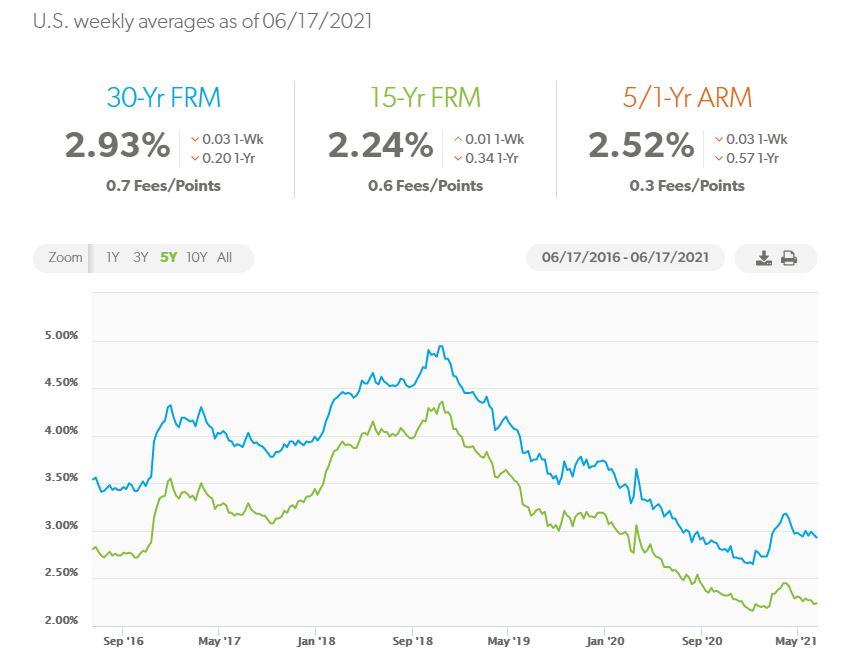

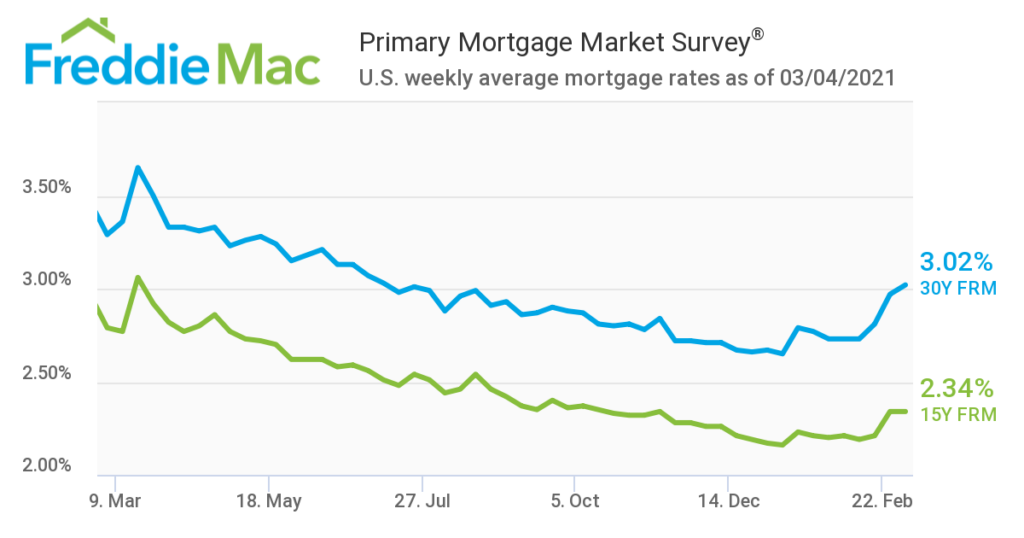

Are mortgage rates heading up or down?

For several years “experts” have been forecasting that mortgage rates were about to rise, but forecasts of an imminent end to low rates are reminiscent of Mark Twain’s alleged comment that reports of his death had been greatly exaggerated.

The 30-year Fixed Rate Mortgage (FRM) reached almost 5% in November 2018, but since then has been in an almost uninterrupted downward trend, with a few short-lived spikes upwards:

Which brings us to the question: is the next move going to be

Inflation (more…)

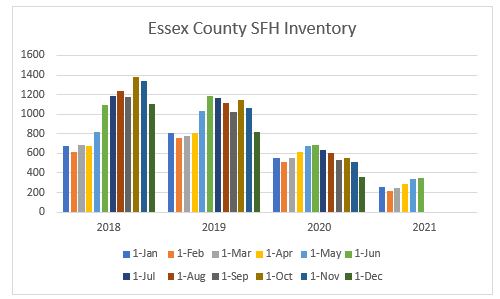

June Housing Inventory: same old same old

Housing inventory for the 34 cities and towns of Essex County in pictures:

Single Family Homes

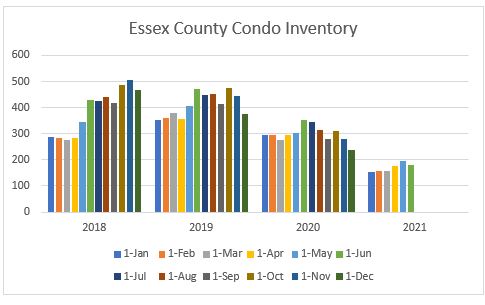

Condos

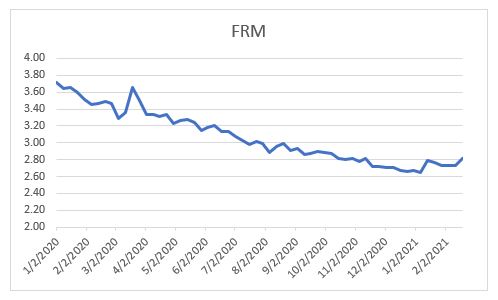

Mortgage rates

After moving up for several weeks the 30-year Fixed rate Mortgage dropped blow 3% again. Note how cheap 15-year mortgages are for those who can afford the extra payment.

Comment (more…)

Hello sub 3% mortgages – again

This week’s drop below 3% – again – reminded me that the only one thing more fraught than commenting on mortgage rates is trying to predict where rates are headed. (see below for some of my posts about mortgage rates.)

After rising steadily from 2.65% at the beginning of the year to 3.18% by the end of March, the 30-year Fixed Rate Mortgage (FRM) has backed off again and this week the rate dropped back under 3%.

Freddie Mac weekly survey

“Party on, dude” says the Federal Reserve

Former Federal Reserve Chair William McChesney Martin, Jr famously said: “The Federal Reserve…is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up.”

This week, current Fed Chair Jerome Powell in effect said “party on, dude.” As the New York Times commented: “The official view of the central bank’s leaders now is that it has been an overly stingy host, taking away the punch bowl so quickly that parties were dreary, disappointing affairs.

The job now is to persuade the world that it really will leave the punch bowl out long enough, and spiked adequately — that it will be a party worth attending. They insist punch bowl removal will be based on actual realized inebriation of the guests, not on forecasts of potential future problematic levels of drunkenness.”

Chairman Powell’s comments

“We will continue to provide the economy the support that it needs for as long as it takes.”

“We’re not going to act pre-emptively based on forecasts for the most part, and we’re going to wait to see actual data. And I think it will take people time to adjust to that, and the only way we can really build the credibility of that is by doing it.”

“People start businesses, they reopen restaurants, the airlines will be flying again — all of those things will happen, and it will turn out to be a one-time bulge in prices, but it won’t change inflation going forward.”

Interest rates and inflation

The big questions overhanging financial markets are what will happen to inflation and to interest rates. (more…)

Goodbye sub 3% mortgages

It was only last July that the 30-year Fixed Rate Mortgage (FRM) dropped below 3% for the first time and this week it moved back above 3% again, following the direction of the 10-year Treasury Note (10T).

Mortgage Rates are Rising

On January 9th I published Are mortgage rates about to rise? which started with:

“Following the Georgia Senate election results, which gave control of the Senate to the Democrats, along with the House of Representatives and the White House, the yield on the 10-year Treasury Note (10T) – the most sensitive to increased Government spending – jumped from 0.93% on Monday to 1.13% on Friday, based upon the expectation that increased Government spending would lead to more borrowing which would need higher interest rates to attract investors.”

Since then the yield on 10T has climbed further, spending this week around the $1.30 level before closing yesterday at $1.34.

Why does this matter for mortgage rates? Because the rate on the 30-year Fixed Rate Mortgage (FRM) is based upon an extra yield – spread – that investors require over that available on 10T. The national average reported on Thursday ( based on rates from Monday-Wednesday) was 2.81%, up from the record low of 2.65% in January, and indications are that the rate will rise again next week.

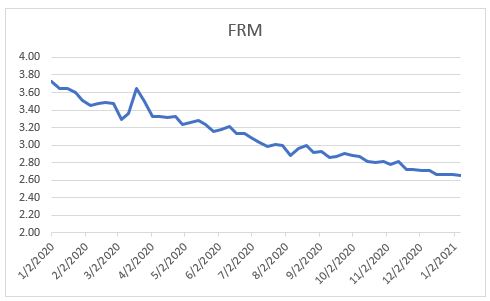

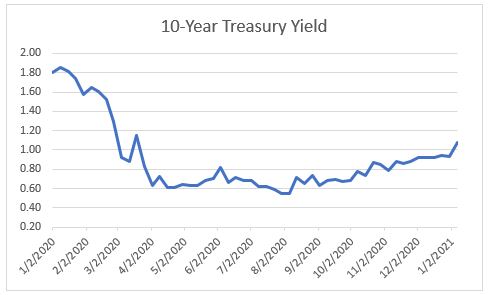

Here are three charts:

The FRM since the beginning of 2020:

The 10T yield:

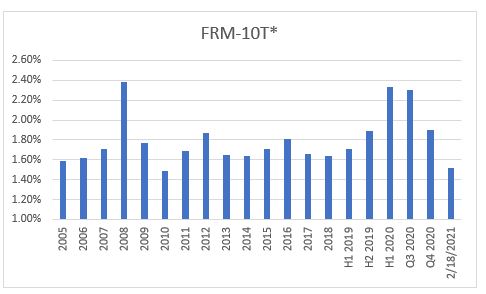

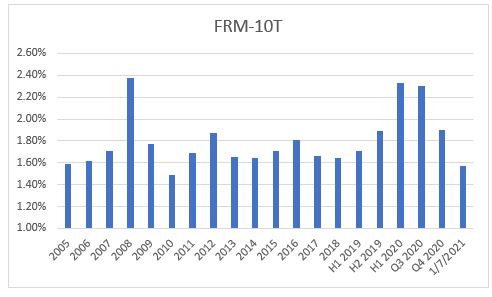

And the Spread between the two (this chart starts in 2005):

For most of the last 15 years the spread has been in the 1.6-1.8% range. The major exceptions have occurred during times of financial stress – in the Great Recession of 2008 and in the pandemic of 2020. But when the stress diminishes, the spread returns to its normal range.

I strongly recommend the weekly Market Trends from HSH.com (click HSH.com to subscribe) for really good commentary on the economy and mortgage markets. In this week’s newsletter they write: “As the economy continues to slowly recover from pandemic-interrupted activity, the process is sure to be an uneven one. However, if there’s an accumulation of solid news in a short period, it would be sufficient to lift interest rates a little bit, expanding the distance from previous record lows. In general, that’s what happened this week, and will be the proximate cause of another bump in mortgage rates next week.

To be sure, interest rates can only rise so far at a time when millions remain out of work, the economy hasn’t yet filled in the output gap caused my pandemic-related interruptions in economic activity and the Fed remains steadfastly committed to low-rate and extraordinary monetary policies. But market-engineered interest rates can still move upward, since these rely on investor perspectives about future levels of growth, inflation and hedges against whenever the Fed may start to trim bond buys and consider raising interest rates.”

For the last year the Federal Reserve has been pouring vast amounts of cash into the monetary system, action that has both driven short-term rates down sharply and contributed to a rise in asset prices as seen in a booming stock market. In recent weeks, the market chatter has been more about when interest rates will rise rather than if. And market expectations can be self-fulfilling.

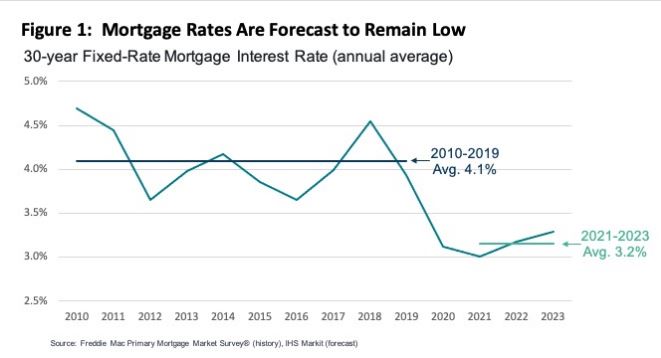

The Mortgage Bankers Association (MBA) published its forecast for mortgage rates this week. While the MBA has a track record of forecasting rising mortgage rates, it is worth noting that the latest forecasts are for the FRM to reach 3.4% by the end of 2021, 3.9% in 2020 and 4.4% in 2023.

While I applaud the bravery of anybody who attempts to make long-range forecasts, I pay little attention to them. HSH, however, has also forecast that the FRM could reach as high as 3.44% this year.

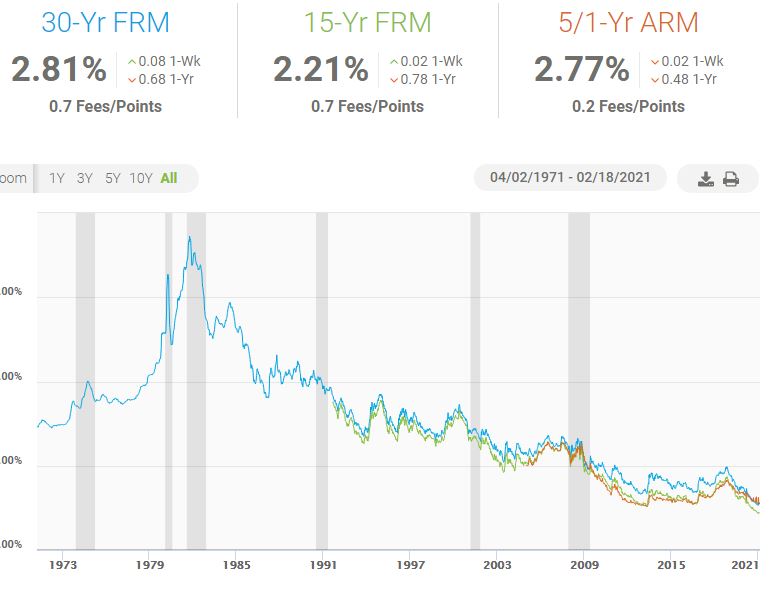

I will conclude as I usually do with this one chart, perhaps the most important one in this article. By any historical standard mortgage rates are extremely attractive. And 15-year mortgages the most attractive of all for those who can afford the higher monthly payment.

Mortgage Markets Return to Normal

Essex County 2021 Residential Property Tax Rates: Town by Town guide

Andrew Oliver

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

www.OliverReportsMA.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

Andrew Oliver

Sales Associate | Market Analyst | DomainRealty.com

REALTOR®

Naples, Bonita Springs and Fort Myers

Andrew.Oliver@DomainRealtySales.com

m. 617.834.8205

www.AndrewOliverRealtor.com

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReports.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

Mortgage rates rise at the fastest pace in months*

On January 9th I published Are mortgage rates about to rise?.

At that time the yield on the US Treasury 10-Year Note (10T) – the benchmark for the 30-year Fixed rate Mortgage (FRM) – had risen to 1.13%, compared with a low of under 0.6% last August.

Well, as of this morning, the yield on 10T is standing at 1.29%. The FRM as of last Thursday’s Freddie Mac survey was 2.73%, but will rise this week, possibly sharply.

My January article concluded: “A number of factors will influence the course of interest rates in the coming months, but at this point it looks as though 2.65% may represent the low point for the FRM.”

I will publish an updated review of mortgage rates this coming Saturday.

*This morning’s headline from CNBC

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

www.OliverReportsMA.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

Andrew Oliver

Sales Associate | Market Analyst | DomainRealty.com

REALTOR®

Naples, Bonita Springs and Fort Myers

Andrew.Oliver@DomainRealtySales.com

m. 617.834.8205

www.AndrewOliverRealtor.com

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReports.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

Are mortgage rates about to rise?

Following the Georgia Senate election results, which gave control of the Senate to the Democrats, along with the House of Representatives and the White House, the yield on the 10-year Treasury Note (10T) – the most sensitive to increased Government spending – jumped from 0.93% on Monday to 1.13% on Friday, based upon the expectation that increased Government spending would lead to more borrowing which would need higher interest rates to attract investors.

Why does this matter for mortgage rates? Because the rate on the 30-year Fixed Rate Mortgage (FRM) is based upon an extra yield – spread – that investors require over that available on 10T. The national average reported on Thursday ( based on rates from Monday-Wednesday) was a record low of 2.65%, but next week will almost certainly see an increase.

Here are three charts:

The FRM since the beginning of 2020:

The 10T yield:

And the Spread between the two (this chart starts in 2005):

For most of the last 15 years the spread has been in the 1.6-1.8% range. The major exceptions have occurred during times of financial stress – in the Great Recession of 2008 and in 2020.

I will add links at the bottom of this article to previous ones describing the relationship between 10T and FRM in more detail.

Meanwhile, note that the FRM is a national average based on rates from Monday-Wednesday, when the yield on 10T was 0.93%, 0.96% and 1.04%; that the yield used in my spread calculation was Thursday’s 1.08%, and that on Friday it was 1.13%. That means that the spread between the latest reported FRM – 2.65% – and Friday’s 10T- 1.13% – was just 1.52%, well below the average in recent years of 1.7%.

A number of factors will influence the course of interest rates in the coming months, but at this point it looks as though 2.65% may represent the low point for the FRM.

Mortgage Markets Return to Normal

Essex County 2021 Residential Property Tax Rates: Town by Town guide

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

Licensed Sales Agent in Florida

www.OliverReports.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReports.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

Would you like a 1% mortgage?

HSBC is offering a 5-year, variable rate mortgage at 0.99%. (more…)

“Mortgage rates low, housing prices high for three years”

CoreLogic has released its Three-Year Housing and Mortgage Outlook and the report says millennials will add substantial demand for housing, while finding low rates and high prices.

“Low mortgage rates, growing numbers of first-time buyers, and gradually rising home values are three housing market trends we expect during the next three years.”

Here is a link to the full Corelogic report: Mortgage and Housing Market Outlook

Conforming Mortgage Loan Limits raised for 2021

Mortgage Markets Return to Normal

How Marblehead’s 2021 Property Tax Rate is Calculated

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

www.OliverReports.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReports.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

Mortgage Markets Return to Normal

Before delving into the details, let me show you the answer, the chart showing the spread – difference- between the 30-year Fixed Rate Mortgage (FRM), as reported weekly by Freddie Mac, and the yield on the 10-year US Treasury Note (10T):

In recent years the 30-year Fixed Rate Mortgage (FRM) has averaged a spread of about 1.7% above the yield on the US 10-year Treasury (10T). (more…)

Mortgage Rates: Another new low

As if in response to my questioning whether mortgage rates were about to rise in Mortgage Rates: another Head Fake or Early Warning? the 30-year Fixed Rate Mortgage (FRM) as reported by Freddie Mac dropped to yet another new low this week of just 2.72%.

This is the moment when you turn to a friend or family member – probably the latter at the moment – and say “when I bought my house in 19xx the rate was – fill in the blank, 7%,8% or whatever.” My highest was 7.3% in 1999. (more…)

Mortgage demand on the increase again

November is not historically a strong season for homebuying, but this one, like the rest of 2020, isn’t following any rules.

Homebuyer demand is surging again, after taking a slight break around the election. (more…)

Mortgage Rates: another Head Fake or Early Warning?

Back in June I wrote Mortgage rate head fake, when mortgage rates jumped but only very briefly.

On Wednesday this week I wrote: “In normal times, the 30-year Fixed Rate Mortgage (FRM) is priced based upon the extra yield investors require over and above that which can be received on the US 10-year Treasury Note (10T). In recent years that extra yield – spread – has averaged 1.7%.

2020, as you may have noticed, has not been normal. In the peak of the disruption to mortgage markets in April the spread reached 2.7%, as the yield on 10T was driven sharply lower, dropping from 1.8% at the beginning of the year to as low as 0.55%.

But recently, the yield has been climbing and now approaches 1%. And the spread over 10T has been under 2% for the last three weeks.”

Here is a chart of the spread in recent years and by quarter in 2020: (more…)

Recent Comments