Will the Federal Reserve show chutzpah today?

In my How far Behind the Curve is the Federal Reserve? report last weekend I suggested that the Fed needed to increase its Fed Funds rate by a full 1.0% today to regain control of the inflation narrative and asked if it has the chutzpah to do this.

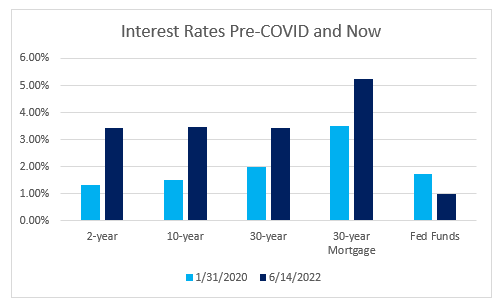

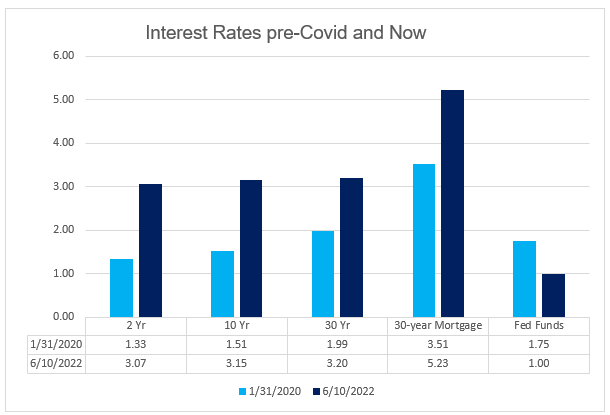

The following table shows clearly that it has been the market fighting inflation by driving up interest rate – while the fed has continued with its easy money policy.

We’ll find out in a few hours how serious this Fed is about getting inflation under control.

And read these recent articles:

How far Behind the Curve is the Federal Reserve?

How quickly are houses selling?

Have Home Sales slowed?

June Housing Inventory: still way below 2020 levels.

Swampscott House on over 1 acre with HUGE potential

Marblehead Neck Oceanfront New Listing

Why are Mortgage Rates so high?

Time to Consider an Adjustable Rate Mortgage

The Federal Reserve and Mortgage Rates

Federal Reserve: “Make me responsible…. but not yet”

How Marblehead’s 2022 Property Tax Rate is calculated

Essex County 2022 Property Tax Rates: Town by Town guide

Guide to Buying and Selling in Southwest Florida

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact me on 617.834.8205 or ajoliver47@gmail.com.

Andrew Oliver, M.B.E.,M.B.A.

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

m 617.834.8205

www.OliverReportsMA.com

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReportsMA.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

__________________

Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com

www.TheFeinsGroup.com

www.OliverReportsFL.com

————

Compass

800 Laurel Oak Drive, Suite 400, Naples, FL 34108

m: 617.834.8205

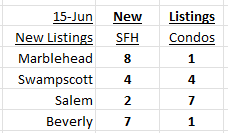

New Listings mid-week June 15

Here are this week’s New Listings:

Click on these links for details: (more…)

How far Behind the Curve is the Federal Reserve?

In March 2020, as the impact of COVID-19 was being felt, the Federal Reserve cut the Fed Funds rate by 50 basis points ( 0.5%) on March 3 and followed that with a 100 basis points (1%) cut on March 15th – a total of 1.5% in under two weeks. This emergency action was decisive and instrumental in preventing a financial disaster. But the economy quickly bounced back with a huge rebound in Q3 2020. The emergency was over.

The Fed, however, kept pumping huge amounts of cash into the economy. Eventually, the market decided that the Fed was behind the curve and market rates took off. Yet the Fed has been slow – make that very slow – to respond. This chart shows interest rates on January 31st 2020, the trading day before COVID-19 was declared to be a public health emergency in the US, and this Friday after the announcement that the Consumer Price Index rose 8.6% in May from a year earlier.

Does anything strike you about this chart? Such as the fact that all the market interest rates are up anywhere from 50% to 130% – and the Fed Funds rate is still way down from its pre-COVID level. (more…)

What Higher Mortgage Rates Mean for the Housing Market

The recent uptick in mortgage interest rates is having a chilling effect on home buyers at the moment, but Wharton real estate professor Benjamin Keys doesn’t expect that to last.

Mortgage interest rates have increased across all categories in the last several weeks, following the Federal Reserve’s first rate hike since 2018 to fight inflation. The interest rate on a 30-year fixed-rate mortgage topped 5% last week, compared with less than 3% a year ago. The jump corresponded with a 40% drop in mortgage applications from a year ago.

“Aside from a few days in 2018, we haven’t seen rates this high persistently since around 2011,” Keys said. “Mortgage rates are the real focus among a lot of people right now, and trying to understand what impact [that is] going to have on housing markets.”

Sky-high rents have been spiraling faster than home prices in the last decade, which will continue to push many Americans toward home ownership. With a fixed-rate mortgage, they can budget a stable monthly housing expense for the next 15 or 30 years. (more…)

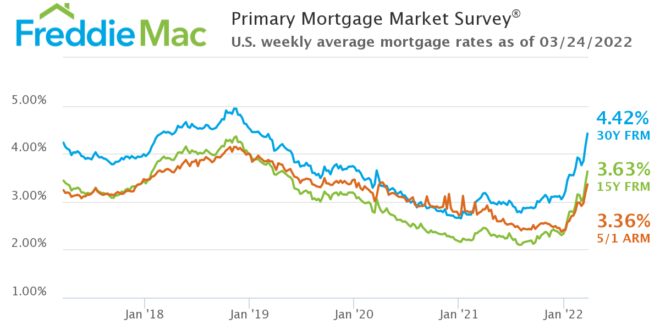

Why are Mortgage Rates so high?

Yes, interest rates are rising and with that so are mortgage rates, but the 30-year Fixed Rate Mortgage (FRM) seems to be about 0.5% higher than I would expect.

First, current rates:

In my recent article The Federal Reserve and Mortgage Rates I explained the link between the FRM and the 10-year Treasury yield (10T). The difference – the spread – has average around 1.7% over time, but with significant fluctuations during periods pf stress.

Here is the chart highlighting the spread at the time of Federal Funds rate changes – and as of this week: (more…)

Time to consider an Adjustable Rate Mortgage

As 30-year mortgage rates (FRM) continue their recent vertical ascent, it is worth considering an Adjustable Rate Mortgage (ARM).

Here are the latest rates:

ARMs got a bad name in the boom that contributed to the Great Recession, but as in so many different situations, that was the result of lax – or no – underwriting standards – think liar loans – and loans with adverse features such as negative amortisation – payments so low, initially, that the loan balance increased over time.

All that changed with the passage of the Dodd-Frank Act in 2010. (more…)

The Federal Reserve and Mortgage Rates

As expected, the Federal Reserve (Fed) increased its Fed Funds Rate (FF) this week by 0.25% to 0.5%, the first increase since 2018.

What does this mean for mortgage rates and why are they rising? The FF rate affects the lending rate for credit cards, auto loans, adjustable rate mortgages, all of which are impacted by banks’ Prime Rate, which moves with the FF rate. Fixed Rate Mortgages – the typical 30-year mortgage – have a longer life and their benchmark is the closest Treasury security, which is the 10-year (10T).

Five charts explain the factors driving mortgage rates. In all cases the numbers are at the dates that the Fed has changed its FF since 2015: 9 increases followed by 5 decreases before this week’s rise. Because the purpose of this article is to show the link between FF, FRM and 10T the dates shown are only those on which the FF rate changed. Bear that in mind when looking at the charts below – they do not attempt to show all the price movements in between the dates shown. (more…)

Federal Reserve: “Make me responsible…. but not yet”

With apologies to St. Augustine the gist from the release this week of the minutes of the last meeting of the Federal Reserve Open Market Committee (FOMC) was that, yes, inflation is worse than we expected, and yes, we need to raise interest rates and, yes, we need to sell some of our huge portfolio of Treasuries and Mortgage-Backed Securities, and we will …soon…I promise.

“Participants observed that, in light of the current high level of the Federal Reserve’s securities holdings, a significant reduction in the size of the balance sheet would likely be appropriate,” the meeting summary stated.

The minutes show concern about inflation and financial stability though members urged “a measured approach” to tightening monetary policy. FOMC members noted that “inflation was beginning to spread beyond pandemic-affected sectors and into the broader economy.”

No kidding. (more…)

Earth to Federal Reserve: What are you waiting for?

As the debate amongst economists continues as to whether the Federal Reserve will raise interest rates 3 times, 5 times or 7 times this year, the Federal Reserve continues to do….nothing.

Giving the market advance warning about changes in monetary policy is an excellent idea, but the lack of flexibility from the Fed is alarming. The Fed has consistently said that its decisions as to the timing of the end of its bond buying program – which has glutted stock and real estate markets with cash – and the start of the “lift-off” in interest rates would be “data dependent.”

Well, my question is this: what data are you seeing Mr. Powell that the rest of us are missing? And by the rest of us I mean professional and award-winning economists – and me..

In March 2021, 11 months ago, Chairman Powell said: “We’re not going to act pre-emptively based on forecasts for the most part, and we’re going to wait to see actual data. And I think it will take people time to adjust to that, and the only way we can really build the credibility of that is by doing it.”

Also in March 2021, I published “Party on, dude” says the Federal Reserve which included:

Former Federal Reserve Chair William McChesney Martin, Jr famously said: “The Federal Reserve…is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up.”

This week, current Fed Chair Jerome Powell in effect said “party on, dude.” As the New York Times commented: “The official view of the central bank’s leaders now is that it has been an overly stingy host, taking away the punch bowl so quickly that parties were dreary, disappointing affairs.

The job now is to persuade the world that it really will leave the punch bowl out long enough, and spiked adequately — that it will be a party worth attending. They insist punch bowl removal will be based on actual realized inebriation of the guests, not on forecasts of potential future problematic levels of drunkenness.”

I just hope that those attending Mr. Powell’s prolonged party are not planning to drive home.

In that March article I also wrote: “The test for the Fed will come in future months as the economy recovers. The market may demand higher interest rates, even as the Fed will want to keep them low to finance continuing federal deficits.”

By June 2021 I was writing: “Should inflation prove to be more persistent than the Fed expects, then it is likely that the Fed will have to start to increase interest rates sooner and move them up more quickly than it currently expects. And mortgage rates would follow.

I have to admit that I struggle to understand how low interest rates, which boost asset classes such as stock prices and real estate, are helping to boost employment. Lower interest rates benefit those who own assets which appreciate.

I would like to see the Fed start to reduce (taper) its bond buying, while encouraging Congress to focus on removing barriers to employment – by providing increased child care allowances, for example. In other words, deal directly with the problem rather than hoping that benefits will trickle down somehow.”

And my most recent post on this subject was Can the Federal Reserve prevent a Recession? in which I wrote: “Since World War II there has been a consistent pattern of the Federal Reserve hiking interest rates to control inflation and thereby triggering a recession. With the Fed finally acknowledging in late November that inflation was not transitory and committing to end its bond buying spree and also raise interest rates, will it be able to avoid a recession? Can this time be different?”

I also wrote: “It is important to understand that the Fed controls short-term rates and that mortgage rates are based upon the yield of the 10-year Treasury, where the yield is set by market demand. I have been forecasting – guessing – that mortgage rates will reach 4% this year as I expect that interest rates will need to be raised aggressively to ward off stubbornly persistent inflation. But if the result is indeed a recession later this year then interest rates may ease back later.

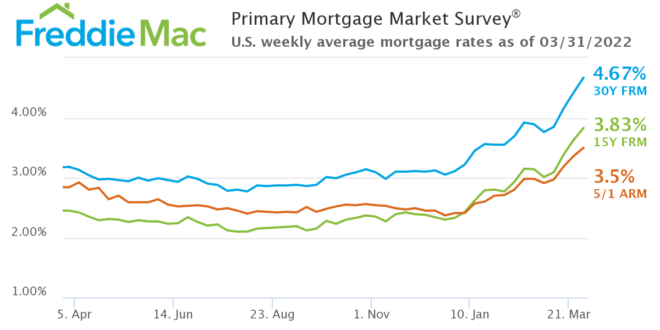

The chart below shows that the 30-year mortgage rate id now back to its pre-COVID level and is set to move higher next week – unless Mr. Putin decides to invade Ukraine, an action which would likely drive investors to buy Treasuries and force rates down in the immediate term.

Summary

The danger of being slow to end the bond buying program and slow to increase short-term interest rates is that the Fed will also be slow to lower rates if economic growth and inflation slow – and thus cause a recession. Right now the US economy is expanding rapidly and is fairly close to the current level of full employment. I hope that the Fed manages successfully to manage interest rates to slow down the economy without driving it into recession. An early 50 basis point rise in the Fed Funds rate would make me more confident that it will succeed.

Read these recent reports:

February Inventory – Marco? Marco? Where are you?

How Marblehead’s 2022 Property Tax Rate is calculated

Essex County 2022 Property Tax Rates: Town by Town guide

Essex County 2022 Commercial Property Tax Rates: Town by Town guide

Guide to Buying and Selling in Southwest Florida

Andrew Oliver, M.B.E.,M.B.A.

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

m 617.834.8205

www.OliverReportsMA.com

Andrew@OliverReportsMA.com

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReports.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

__________________

Andrew Oliver

m. 617.834.8205

www.AndrewOliverRealtor.com

www.OliverReportsFL.com

Can the Federal Reserve prevent a Recession?

The housing market is driven by the balance between supply and demand. Supply cannot be increased significantly quickly, so the only way for the booming housing market to slow is if demand drops. And the most likely causes for a drop in demand are either a major geopolitical development – such as Russia invading Ukraine and the US and its NATO partners deciding to respond militarily – or a recession.

Since World War II there has been a consistent pattern of the Federal Reserve hiking interest rates to control inflation and thereby triggering a recession. With the Fed finally acknowledging in late November that inflation was not transitory and committing to end its bond buying spree and also raise interest rates, will it be able to avoid a recession? Can this time be different?

The Boston Globe recently carried an excellent article on this subject by Jim Puzzanghera: ‘A hellishly difficult task.’ Can the Federal Reserve lower inflation without causing a recession?

“The virus is unpredictable. People’s responses to the virus are unpredictable. It’s not a garden variety business cycle by any means,” said Donald Kohn, a senior fellow at the Brookings Institution think tank who served as Fed vice chair from 2006-10. “It’s much harder to peer into the future and know how to calibrate your monetary policy.”

Bernard Baumohl, chief global economist at the Economic Outlook Group, a forecasting firm, was more blunt. “The Fed has a hellishly difficult task right now,” he said. “There is absolutely no history for the Fed to lean on to deal with this kind of inflation.”

Most economists predicted last spring that high inflation would be temporary, pointing to the supply chain problems caused by restarting the US and world economies. But some economists warned the $1.9 trillion COVID aid bill enacted last March risked fueling longer-lasting inflation by pumping too much money into the already recovering US economy.

By last June even I was writing: “Should inflation prove to be more persistent than the Fed expects, then it is likely that the Fed will have to start to increase interest rates sooner and move them up more quickly than it currently expects. And mortgage rates would follow.

The Fed’s two goals of price stability and maximum sustainable employment are known collectively as the “dual mandate.” In explaining its policy of keeping interest rates low – in part by buying large quantities of Treasuries and Mortgage-Backed Securities, the latter helping to keep mortgage rates low – the Fed refers to the still high level of unemployment.

I have to admit that I struggle to understand how low interest rates, which boost asset classes such as stock prices and real estate, are helping to boost employment. Lower interest rates benefit those who own assets which appreciate.

I would like to see the Fed start to reduce (taper) its bond buying, while encouraging Congress to focus on removing barriers to employment – by providing increased child care allowances, for example. In other words, deal directly with the problem rather than hoping that benefits will trickle down somehow.”

Some quotes (more…)

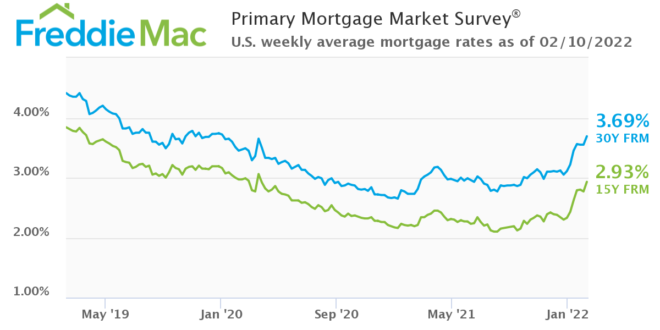

Are Mortgage Rates really under 3%?

When Freddie Mac released its weekly mortgage survey on Thursday it did so with the heading: “Mortgage Rates Drop Below Three Percent Again.”

Which they are not now.

The problem lies with the methodology. Freddie Mac surveys lenders from Monday to Wednesday with the major weighting given to Monday’s rates. As I have explained in many postings over the years (see Mortgage Rates back to 3% – again as an example), the 30-year Fixed Rate Mortgage (FRM) is priced based upon a premium that investors, when they buy pools of mortgages, demand over the yield on the nearest-equivalent US Treasury – which is the 10-year Note (10T). Thus, if the yield on 10T increases from Monday to Thursday – as it did this week – by the time of Thursday’s announcement the FRM may have changed – as it did this week.

Mortgage News Daily had a great article this week and I am going to use their charts. I recommend signing up for their newsletter, a source of great information and opinion. (more…)

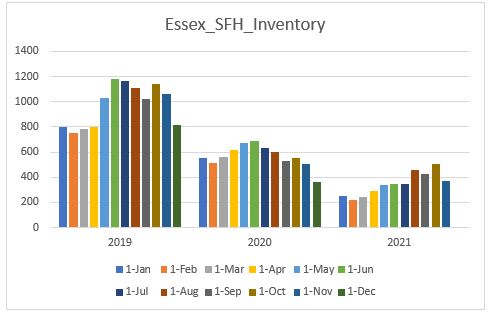

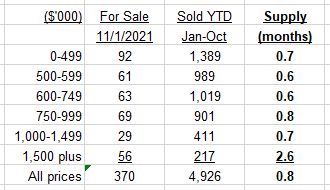

Latest Housing Inventory

After increasing somewhat – albeit from a very low base – during 2021, the seasonal drop-off in late October has been just as sharp as in prior years – and again this is a reduction from a low level.

Single Family Homes

The November 1st SFH inventory number of 370 was a decline of 27% from 2020 and 65% compared with 2019:

Inventory now has less than 1 months’ supply overall and is only over 1 month – but still far below the 6 months deemed to reflect a market in equilibrium – at prices over $1.5 million.

Condos (more…)

Mortgage Rates back to 3% – again

The 30-year Fixed Rate Mortgage ticked back up to 3% this week. I re-read Are Mortgage Rates headed Up or Down? which I published in June and I still think it summarises the situation quite well. Hence I have included the link rather than repeating the arguments.

The proximate cause for the increase in mortgage rates this week was the increase in the yield on the US Treasury 10-year Note. The increase started last week (after the Freddie Mac weekly survey, which is collected from Monday-Wednesday) when the Federal Reserve (Fed) confirmed that, if current trends continue, it will start to reduce its purchases of both Treasuries and Mortgage Backed Securities (MBS) soon and aim to end purchases by the middle of 2022.

At the same time, we saw a rate increase in Norway – the first in Europe- following earlier increases in Brazil and South Korea. And while the Fed continues to state that it will not consider actual rate increases (I am not sure why they refer to it as “lift off”- sounds like rocket-speed increases which it will not be) until after the end of the bond purchases, investors noticed a shift in the number of members forecasting a rate increase in 2022 rather than 2023.

And inflation continues to run hot. The Fed thinks this is transitory, but many others fear that it will be sustained forcing the Fed to raise rates sooner than it currently anticipates.

The Numbers (more…)

Flood Insurance Changes Coming Oct 1

Changes are coming to the flood insurance policy sector taking effect October 1st on new policies and April 1, 2022 on any outstanding renewal policies. I will write further as more details are revealed but these are the highlights from the FEMA Risk Rating 2.0 announcement:

1. Flood zones and Elevation Certificates will no longer be a rating factor (Flood zones will still be present for mortgage purposes)

2. Elevation Certificates will no longer be needed to determine rate

3. No more preferred rate tables for X,B,C Flood zones

4. Flood Vents (2 openings on 2 walls on lowest level) will no longer provide significant savings

5. Machinery on ground floor will impact rate (ex:a/c, water heater, washer/dryers)

6. Grandfathering: (more…)

Mortgage refinancing just got cheaper

The Federal Housing Finance Agency (FHFA) announced that Fannie Mae and Freddie Mac will eliminate the Adverse Market Refinance Fee for loan deliveries effective August 1, 2021.

Lenders will no longer be required to pay Fannie and Freddie a 50-basis point fee when they deliver refinanced mortgages. The fee was designed to cover losses projected as a result of the COVID-19 pandemic. “The success of FHFA and Fannie and Freddie’s COVID-19 policies reduced the impact of the pandemic and were effective enough to warrant an early conclusion of the Adverse Market Refinance Fee.” FHFA’s expectation is that those lenders who were charging borrowers the fee will pass cost savings back to borrowers.

“Santa Claus has come early for homeowners looking to refinance their mortgages,” said Greg McBride, chief financial analyst for Bankrate.com. “The fee had often resulted in an increase of one-eighth percentage point in rate.” (more…)

Recent Comments