The Federal Reserve and Mortgage Rates

As expected, the Federal Reserve (Fed) increased its Fed Funds Rate (FF) this week by 0.25% to 0.5%, the first increase since 2018.

What does this mean for mortgage rates and why are they rising? The FF rate affects the lending rate for credit cards, auto loans, adjustable rate mortgages, all of which are impacted by banks’ Prime Rate, which moves with the FF rate. Fixed Rate Mortgages – the typical 30-year mortgage – have a longer life and their benchmark is the closest Treasury security, which is the 10-year (10T).

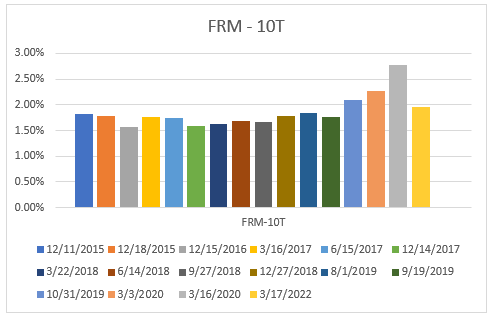

Five charts explain the factors driving mortgage rates. In all cases the numbers are at the dates that the Fed has changed its FF since 2015: 9 increases followed by 5 decreases before this week’s rise. Because the purpose of this article is to show the link between FF, FRM and 10T the dates shown are only those on which the FF rate changed. Bear that in mind when looking at the charts below – they do not attempt to show all the price movements in between the dates shown.

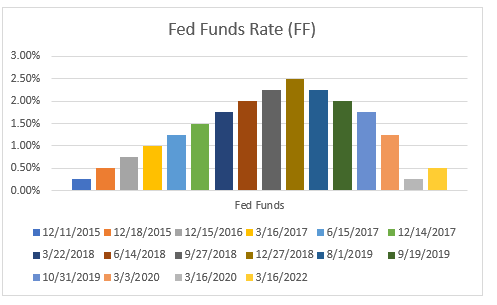

Fed Funds Rate (FF)

The Fed Fund Rate is the rate at which banks lend to each other overnight. The rate was slashed in 2020 in response to the outbreak of COVID-19 and the fear that financial markets would freeze. Many of us have felt that the Fed kept rates too low for too long.

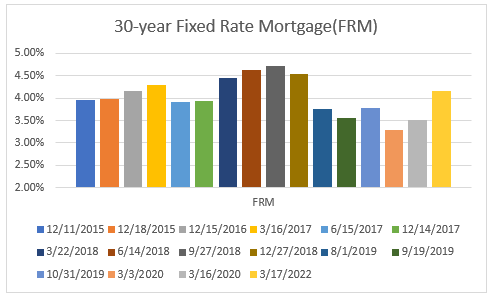

30-year Fixed Rate Mortgage (FRM)

The FRM reached nearly 5% in late 2018 and spent most of 2021 hovering either side of the 3% mark, before jumping by a full percentage point in 2022.

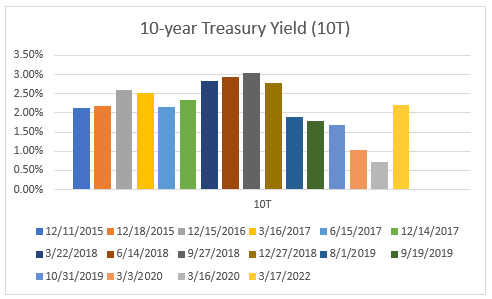

10-year Treasury yield (10T)

The yield on the 10T is influenced by two major factors: the outlook for the economy (expanding businesses invest creating demand for money) and geopolitical events – the US dollar and US Treasuries are seen as a safe haven during times of uncertainty.

After reaching 3.2% in late 2018, the yield on 10T had already dropped to under 2% in early 2020 before the emergency rate cut and Quantitative Easing program in response to the outbreak of COVID drove the yield to around 0.6%. As markets and the economy recovered, so the yield on 10T has also recovered to over 2%.

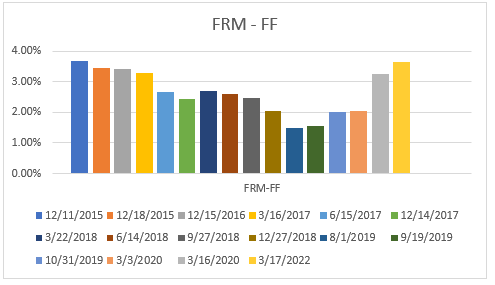

The spread, or difference, between FRM and FF

If there were a link between FF and FRM it would show up in this chart. In fact, the spread dropped from 3.7% in 2015 to 1.5% in 2019 before increasing to the current 3.7% again, demonstrating that there is no direct link between FF and FRM

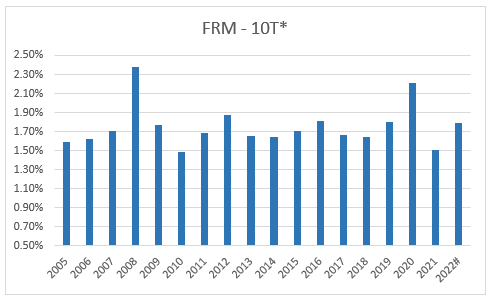

The spread, or difference, between FRM and 10T

We see more consistency between FRM and 10T where, apart from the disruptions caused by the fed’s emergency measures in 2020-21, the spread has been in a much tighter range of 1.5% to 1.8%.

Indeed, over the last several years the spread has been very stable averaging around 1.7%.

Comment

Conventional mortgages are bundled and sold to investors, who require a risk premium – higher yield – over that offered by 10T.

As can be seen, that premium – spread – has been remarkable constant over recent years. It does fluctuate from time to time – the yield on 10T tends to move quickly at times – but in recent years has always comes back to that 1.7% level.

The reason that mortgage rates have been rising in recent months, therefore, is that the yield on 10T has been rising.

And read these recent articles:

Federal Reserve: “Make me responsible…. but not yet”

Earth to Federal Reserve: What are you waiting for?

Can the Federal Reserve prevent a Recession?

February Inventory – Marco? Marco? Where are you?

How Marblehead’s 2022 Property Tax Rate is calculated

Essex County 2022 Property Tax Rates: Town by Town guide

Guide to Buying and Selling in Southwest Florida

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact me on 617.834.8205 or [email protected].

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of Oliver ReportsMA . He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Sale, Beverly, Lynn and Swampscott.”

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

m. 617.834.8205

www.OliverReportsMA.com

————————–

Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

[email protected]

www.TheFeinsGroup.com

www.OliverReportsFL.com

Compass

800 Laurel Oak Drive, Suite 400, Naples, FL 34108

m: 617.834.8205