Federal Reserve in Fantasyland: Implications for Housing Market

Immediately following the issuance of the Federal Reserve’s decision on Wednesday to increase the Fed Funds rate by 0.75% and the accompanying, optimistic statement and press conference, both bonds and equities rallied strongly, leading some to think – hope – that the worst was over in markets.

And then came Thursday, when equities resumed their plunge and bonds rallied further – on the belief that a recession was now likely. (See my Are we already in a recession?).

For my part, were it not so serious I would have allowed myself a louder chuckle as I heard Chair Powell say that the Fed would be “data-dependent” – and then forecast that inflation – using the Fed’s preferred measurement – would be 5.2% this year, 2.6% in 2023 and 2.2% in 2023. Based upon what “data” exactly? And what does all this mean for the housing market?

Fantasyland

If you google “Federal Reserve and Fantasyland” you will get a lot of hits. And while many of the comments from Wall Street insiders – particularly those working for investment banks who tend to be optimists – were supportive of the Fed, many of those with perhaps more objectivity were in the fantasyland camp.

The response to COVID

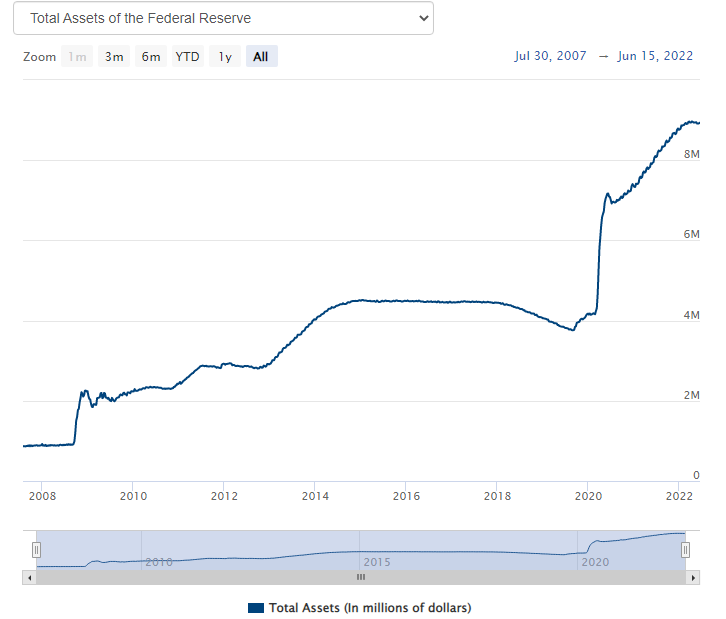

The world’s economy faced a major shock and challenge with the outbreak of COVID. In response the Fed acted swiftly – cutting the Fed Funds rate by 1.5% in two weeks in March 2020 – and with shock and awe – a huge program of Quantitative Easing – injecting vast amounts of liquidity into markets. The Fed became the main buyer of Government and Mortgage-Backed Securities (MBS) and its balance sheet doubled from $4 trillion to over $8 trillion:

By the third quarter of 2020 the economy was rebounding strongly, aided by some $2 trillion from the 2020 American Cares Act. And then in 2021, when the Fed was still injecting cash into the system, Congress passed the $2 trillion American Rescue Plan.

And where did all this liquidity go? Into the stock market and the housing market, both of which enjoyed booms. The slogan in the stock market was TINA (There Is No Alternative) because interest rates were close to zero (but still above zero unlike many other countries).

Looking back now, it beggars belief that the Fed, with access to the finest economic minds in the country, did not foresee that pumping trillions of dollars into a rapidly growing economy might lead to inflation. And yes, I know about supply chain problems and the Russian invasion of Ukraine, but as somebody once said – there’s always something. What I find especially frustrating is that the problems being faced today were both predictable – and predicted. Economic giants such as Larry Summers and Mohamed El-Erian were calling for the Fed to reverse its policy a year ago, as was a somewhat less giant-like economic figure – me. Looking back on my posts I started warning of inflation risks in March 2021 and called for the Fed to start reversing its QE program in June 2021.

The market still leads the Fed

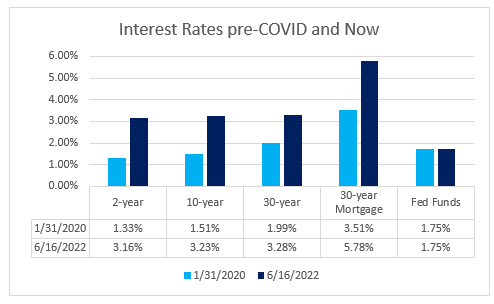

Despite this week’s increase, the Fed remains behind the curve, with the Fed Funds rate just now back to pre-COVID levels while market rates have jumped – in many case more than doubling.

Where to now?

OK rant over, so now where doe the Fed go and what does that mean for the housing market? Fed’s Powell confirmed on Friday that the Fed was “acutely focused on returning inflation to our 2 percent objective.” I think the charts above have shown not only how far behind markets the Fed is but also how much excess liquidity continues to slosh around in markets. We also have to acknowledge that so much of what is driving inflation is beyond the control of either the Fed or Congress or the Administration.

But it does seem that the Fed, albeit 6-12 months late, is now committed to doing what it can to drive inflation back down to 2%. And what it can do is raise interest rates and drain some liquidity from the system by selling some of its gargantuan holding of Treasuries and MBS. It is important here to understand that the Fed Funds rate set by the Fed is used by banks to set a lot of consumer interest rates – credit cards, auto loans, etc. Mortgage rates, in general, are priced off the 10-year Treasury and that rate is set by the market on the same basic economic formula which drives home prices – supply and demand. In other words, increasing Fed Funds rates do not mean that mortgage rates will rise – just as well since they have doubled from last year’s lows.

What this means is that, just as the yield on 10T has more than doubled since pre-COVID while the Fed Funds rate is unchanged, so the Fed Funds rate can increase sharply – the Fed is forecasting it will reach 3.4% this year, also double its pre-COVID level – without necessarily impacting the yield on 10T.

That will depend upon the economic outlook. Ironically, perhaps, the more determined the Fed is to drive down inflation – even at the cost of a recession and higher unemployment – the greater the chance that the yield on 10T – and by extension the FRM – will decline – at some point.

The housing market

Well, of course, there is no one housing market. But general trends do have an impact on local markets. The more stories that appear about increasing inventories, rising mortgage rates, threats of a recession ( I’ll stop there), the more buyers everywhere will start to pull back. Bear in mind the old saying in real estate that buyers buy with emotion – and the emotion today is on the depressing edge of the spectrum.

Against that, we are coming off a period when active inventories in many markets – especially ours – have been extraordinarily low.

When COVID hit in 2020 the reaction was for activity to slow dramatically, but prices didn’t. There is a chance – which is not a forecast – that the recession will be quite short, as consumers throttle back a bit, but still have substantial reserves of liquidity built up over the last two years.

Investors in the stock market can put money to work over time – buying a little each month, for example. That does not work in the housing market where it is one and done.

In recent years, my advice when asked has been quite straight forward: if the house meets your needs and you plan to live there for the foreseeable future and you can afford it – buy it. But don’t compromise. Matt Dolan of Team Harborside told me once that the TH approach to a house is threefold:

1) Location – you can’t change that

2) Flow – does the house work for the way you live?

3) Condition

You can’t change 1, it is difficult to change 2 – but you can change 3.

Approach to the market

After a couple of years when houses were being sold, sight unseen, for sometimes obscene premiums to listing prices, it is reasonable to expect some equilibrium to return to the housing market this summer – bear in mind that if the Q2 data does show a recession that news will not hit the headlines for another month. And cash buyers may not be quite so flush after a 30% plus decline in the NASDAQ this year leaving many stock options, especially in the hottest sectors, under water.

And I repeat: if the house meets your needs and you plan to live there for the foreseeable future and you can afford it – buy it. And you may have greater choices in the coming weeks and months.

And read these recent articles:

Are we already in a Recession?

How far Behind the Curve is the Federal Reserve?

How quickly are houses selling?

Have Home Sales slowed?

June Housing Inventory: still way below 2020 levels.

Time to Consider an Adjustable Rate Mortgage

The Federal Reserve and Mortgage Rates

How Marblehead’s 2022 Property Tax Rate is calculated

Essex County 2022 Property Tax Rates: Town by Town guide

Guide to Buying and Selling in Southwest Florida

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact me on 617.834.8205 or ajoliver47@gmail.com.

Andrew Oliver, M.B.E.,M.B.A.

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

m 617.834.8205

www.OliverReportsMA.com

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReportsMA.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”

__________________

Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com

www.TheFeinsGroup.com

www.OliverReportsFL.com

————

Compass

800 Laurel Oak Drive, Suite 400, Naples, FL 34108

m: 617.834.8205